Governance professionals report on their board's structures and processes for overseeing ESG matters, and how well equipped they are for that role

Risk oversight is a core responsibility for all boards and addressing ESG-related matters is rapidly becoming a core part of risk oversight. In today's changing political, legal and physical climates, companies and their boards face growing scrutiny from investors, customers, employees, regulators and others in terms of how they are monitoring and responding to ESG issues.

For boards to be able to oversee ESG matters effectively, they need to have the right committee structures and reporting processes. They need to have access to the right information and they need to have the right expertise and experience. They also need to be asking the right questions and having relevant discussions. For many, adapting to a more fully realized ESG oversight role presents a steep learning curve. As in other governance areas, however, much can often be learned by looking at how peers are addressing these challenges.

In this special report we present findings from a survey conducted among governance professionals such as general counsel and corporate secretaries.

Their responses give insight into, among other things, which part of the board is taking responsibility for ESG oversight, when ESG discussions happen and on what topics, how the board’s ESG oversight capabilities are viewed and how professionals think boards’ ESG oversight could be improved.

Key findings

Almost half (43 percent) of respondents say their full board has primary oversight of ESG issues. The next-most common response is the nominating and governance committee, cited by 25 percent of respondents.

Almost a third (30 percent) of respondents say committees with ESG oversight report to the main board on those issues on an ad hoc basis.

Globally, 80 percent of respondents report an increase in the frequency of main-board discussions of ESG issues, compared with two years ago.

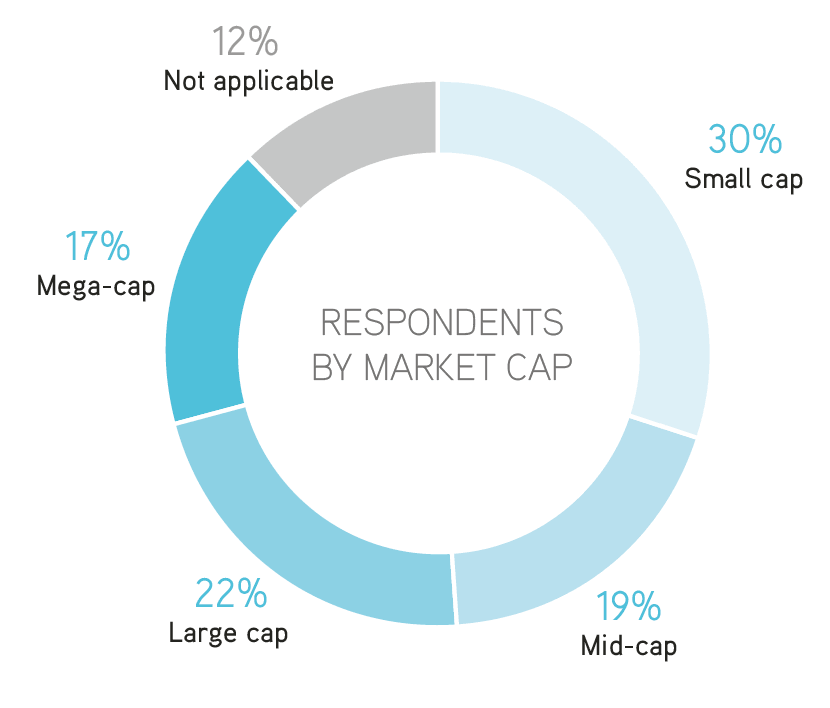

Almost all respondents at mega-caps (94 percent) say board diversity has been discussed over the past year, compared with 76 percent of those at large-cap companies, 85 percent of those at mid-caps and 63 percent of those at small caps.

More than half (55 percent) of respondents say that in the past 12 months, investors have asked questions about the board’s governance structure and processes around ESG issues.

Respondents at mega-cap companies give the highest average rating of their board’s ability to oversee relevant ESG matters (8.3 out of 10).

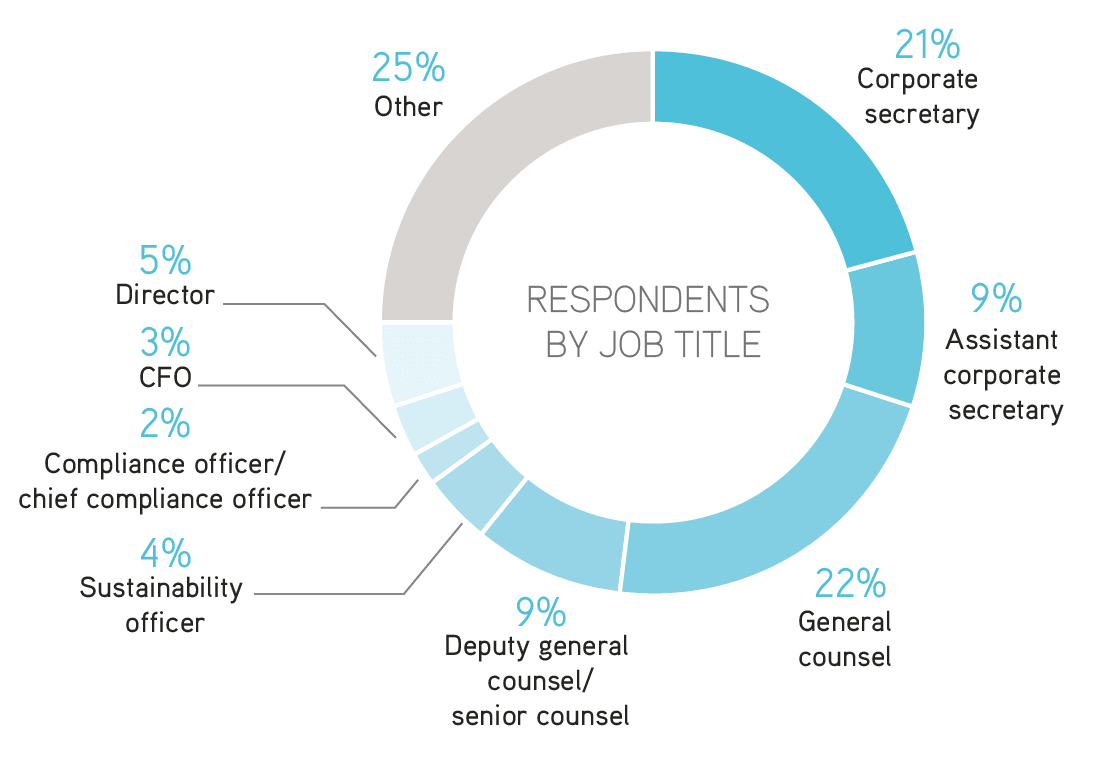

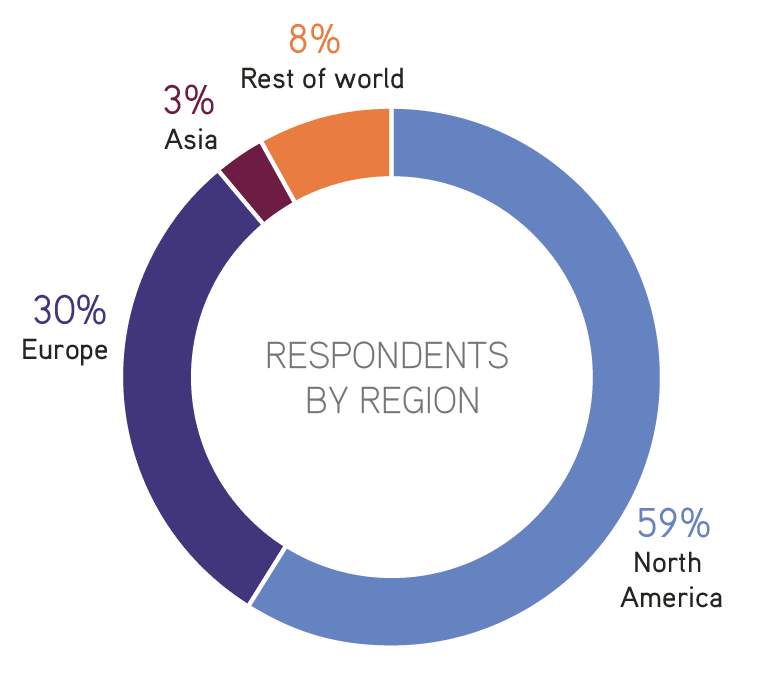

Survey demographics This report is based on the findings from an online survey conducted between December 2021 and February 2022.

Total number of respondents: 210