Governance professionals provide valuable insights into their work and how companies are supporting their needs

A successful entity management program is key to ensuring a company’s often-complex business network has an efficient structure in which all components comply with local law and regulations. Beyond that, it is necessary to support M&A, minimize entity costs and ensure consistent governance across the organization.

Entity management is an area that gains greater attention at larger companies, which often have more extensive networks of subsidiaries, but it is an essential function for firms of almost any size. The challenges and opportunities it presents include navigating a variety of jurisdictions with their own legal and compliance demands, getting buy-in from employees and directors across diverse entities, maintaining sufficient resources and using technology in the most effective and evolving ways.

In this special report, we present the results of global research conducted among governance professionals such as general counsel, corporate secretaries and their teams. Respondents provide insights – analyzed globally and by region and cap size – on who takes charge of entity management work, where their efforts are targeted, how their budgets, headcounts and use of technology are changing, the most difficult regions to work in and how they view their companies’ efforts.

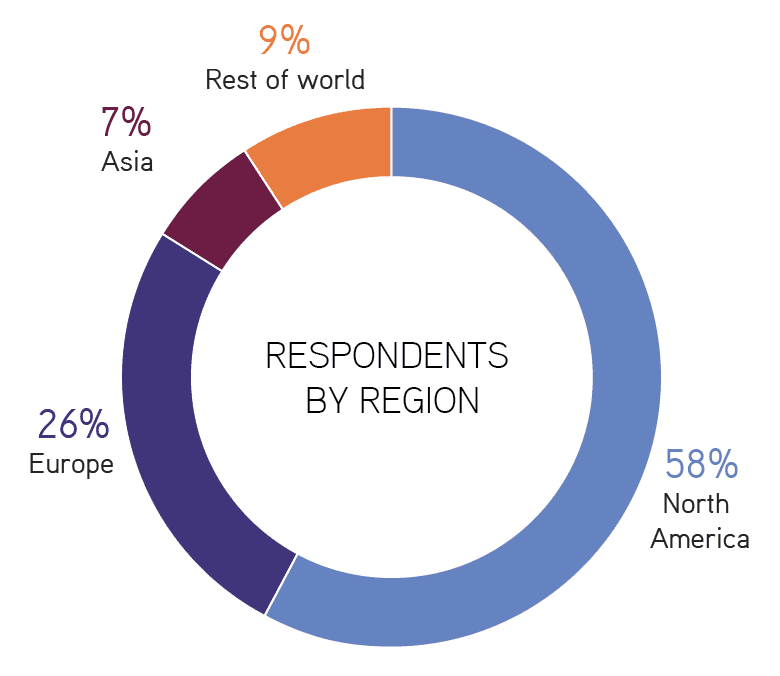

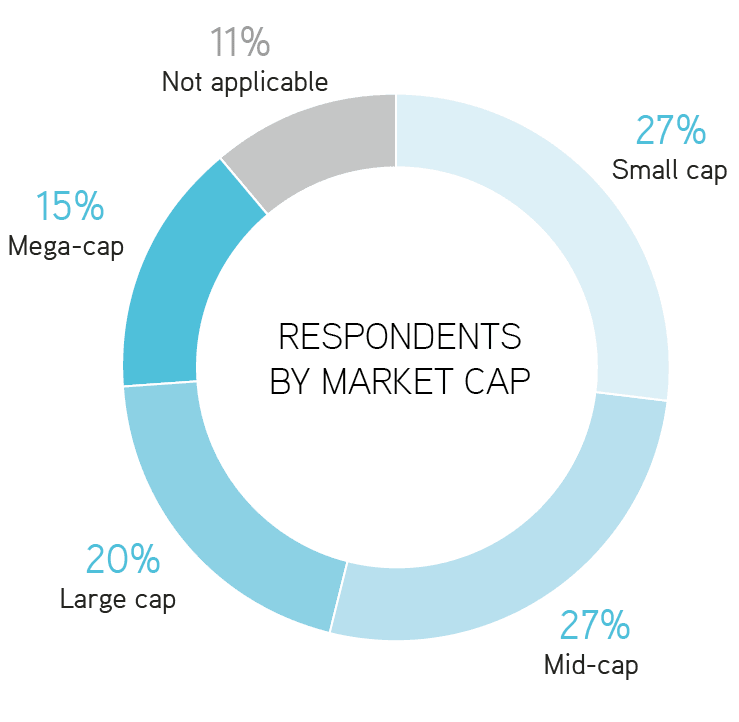

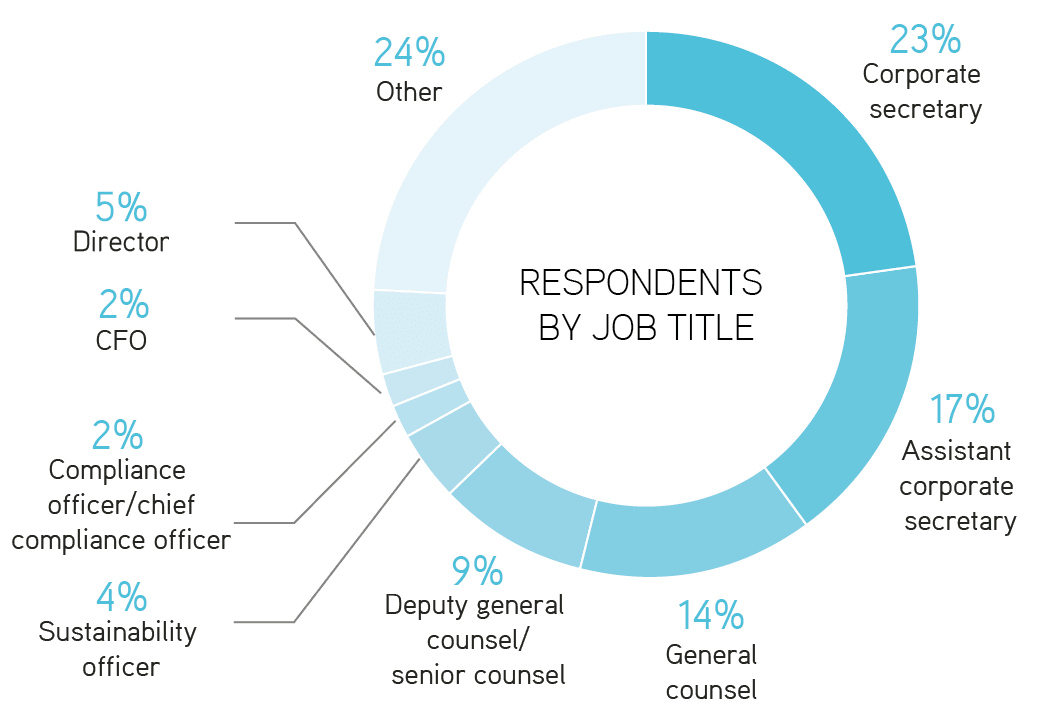

Total number of respondents: 221

Survey demographicsThis report is based on the findings from an online survey conducted between September 2023 and January 2024. A total of 221 respondents participated in the research.

With any core governance function, it is important to know who is responsible for getting the work done and making sure it is effective.

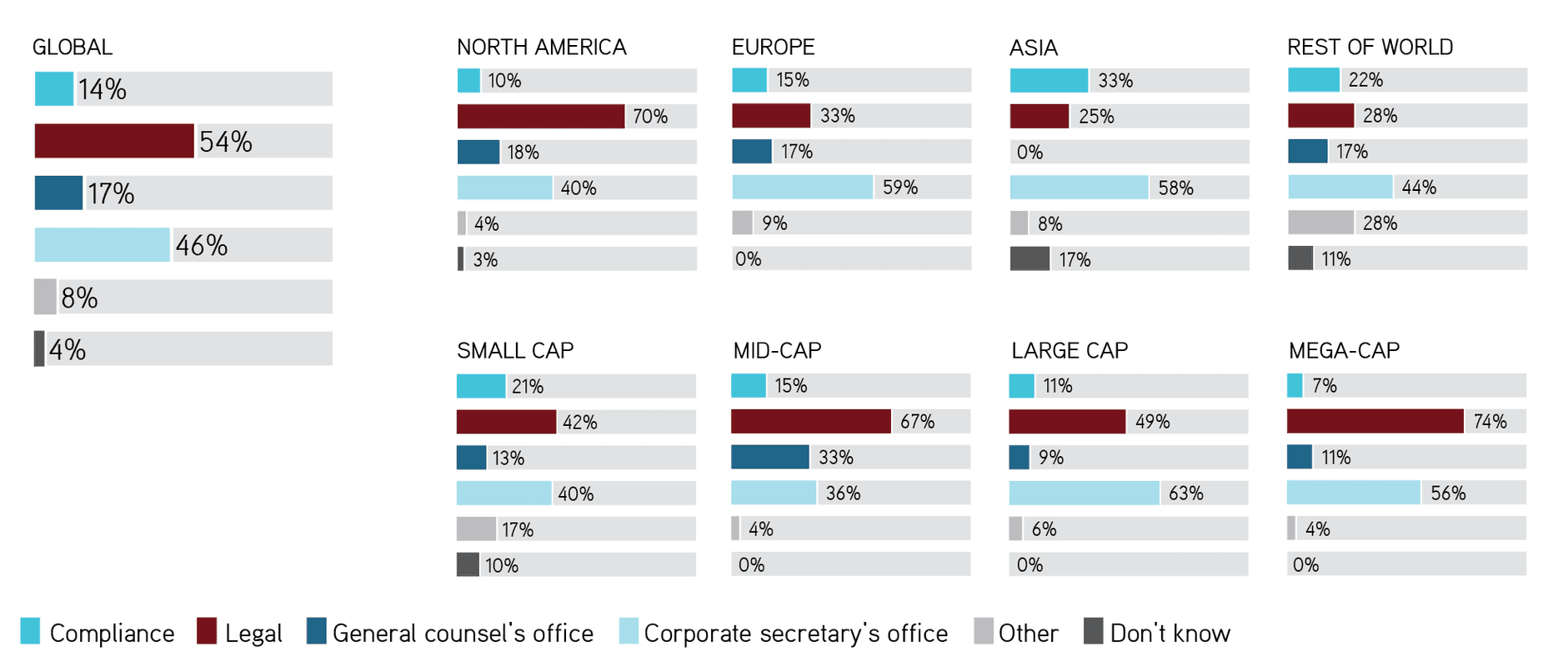

Globally, more than half (54 percent) of respondents say their legal department is responsible for overseeing entity management at their company. This is followed by the corporate secretary’s office, which is mentioned by 46 percent of those taking part in the research. Far fewer point to the general counsel’s office (17 percent) or compliance department (14 percent).

Among respondents in North America, seven in 10 say legal is responsible, with 40 percent saying the corporate secretary’s office, 18 percent mentioning the general counsel’s office and just 10 percent referring to compliance. By comparison, only a third of respondents in Europe name the legal team, while 59 percent say the corporate secretary’s office is responsible.

Respondents at mega-caps (74 percent) are more likely to say their legal team is responsible for entity management than those at mid-caps (67 percent), large caps (49 percent) or small caps (42 percent). Those at large caps are most likely to point to the corporate secretary’s office (63 percent), compared with 56 percent of mega-cap respondents, 40 percent of those at small caps and 36 percent of those at mid-caps.

Entity management takes a substantial amount of effort and expertise, and companies often look outside for help on at least some issues to supplement their internal resources.

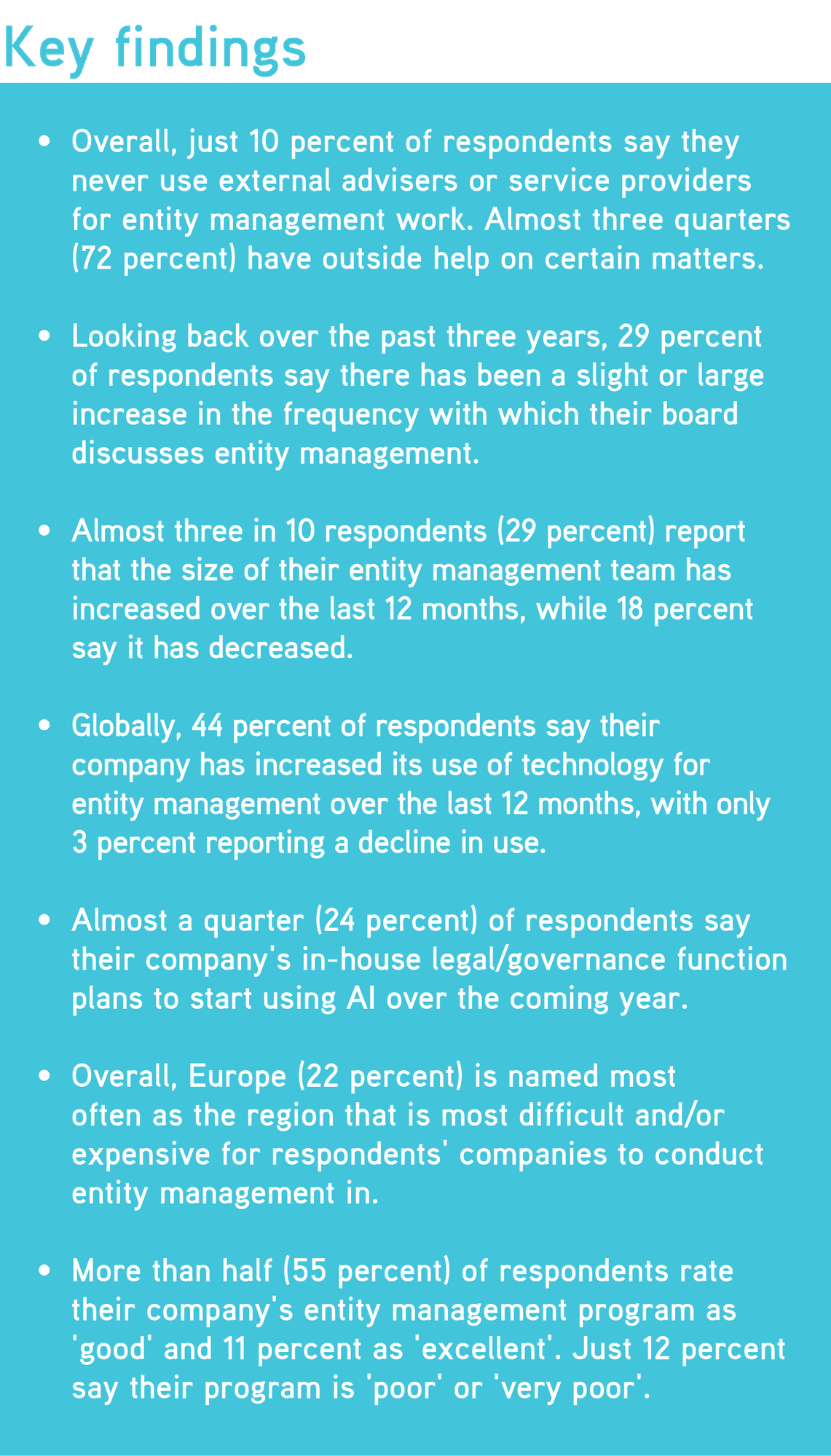

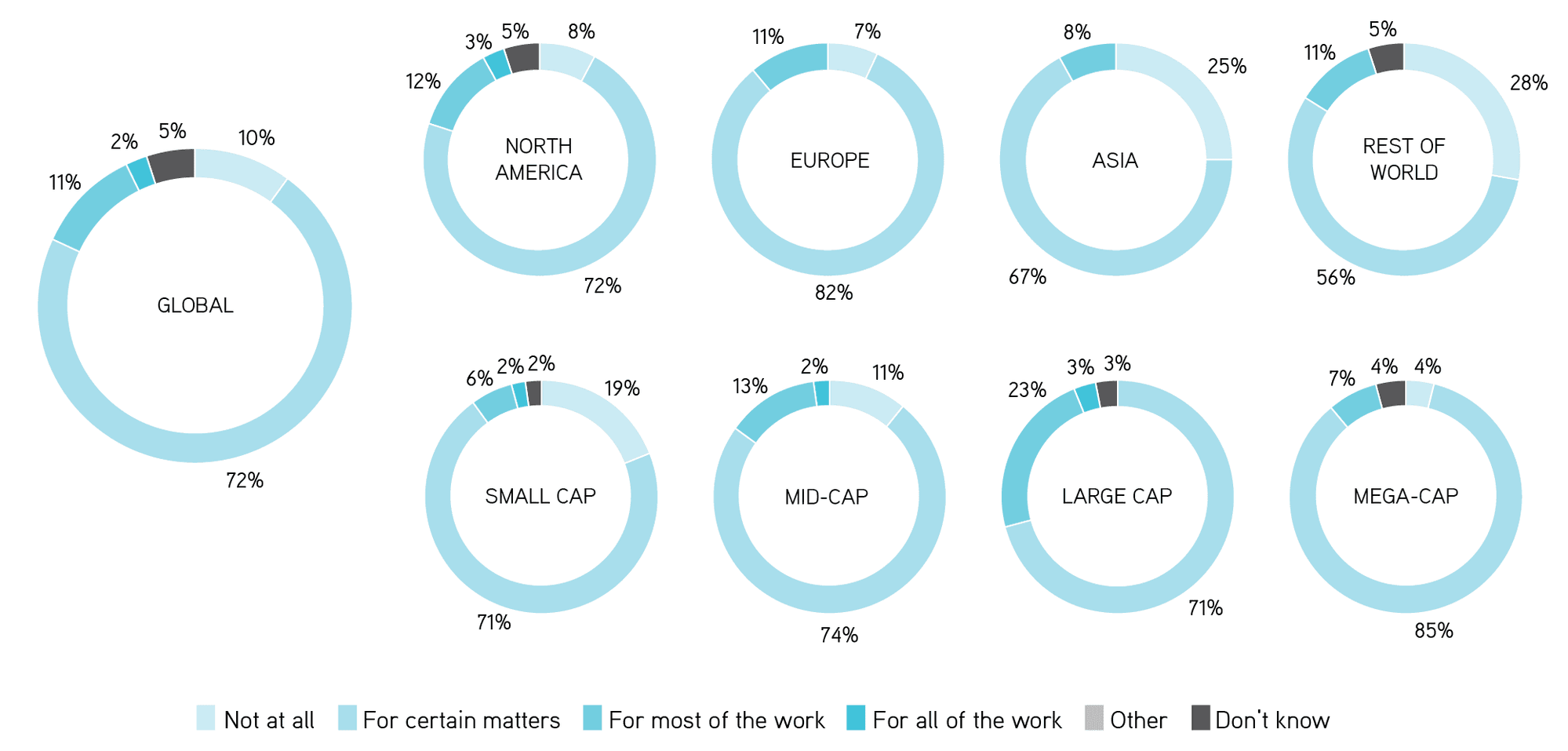

Overall, just 10 percent of respondents say they never use external advisers or service providers for entity management work. Eleven percent say they use outside advisers or service providers for most of the work and a handful (2 percent) use outside help for their entire entity management program. Almost three quarters (72 percent) have outside help on certain matters.

Of course, the size of the organization is important in determining the amount and complexity of work involved in entity management, and this is reflected in the use of external advisers and service providers. Almost one fifth (19 percent) of respondents at small-cap companies say they never turn to outside help, compared with 11 percent of those at mid-caps, none of those at large caps and 4 percent of those at mega-caps.

Almost a quarter (23 percent) of respondents at large-cap companies use external advisers/service providers to carry out most of their entity management work.

Those that turn to external advisers/service providers do so most frequently for subsidiary compliance matters (48 percent). This is followed by M&A (37 percent), regulatory reporting (36 percent), legal entity tracking (27 percent), subsidiary governance (24 percent) and ultimate beneficial owners registration or director and officer issues (22 percent each).

Respondents in Europe more frequently say they use outside advisers/service providers for M&A work (42 percent) than do their counterparts in North America (31 percent).

Bigger organizations tend to have more extensive webs of entities that need to maintain good standing with local laws and regulations. Two thirds of respondents at large-cap companies and 62 percent of those at mega-cap firms say they use external advisers/service providers to handle subsidiary compliance. This compares with 35 percent and 45 percent of those at small caps and mid-cap companies, respectively.

Similarly, 38 percent of respondents at mega-cap firms use outside help for legal entity tracking. This falls to 33 percent, 26 percent and 19 percent of peers at large caps, mid-caps and small caps, respectively.

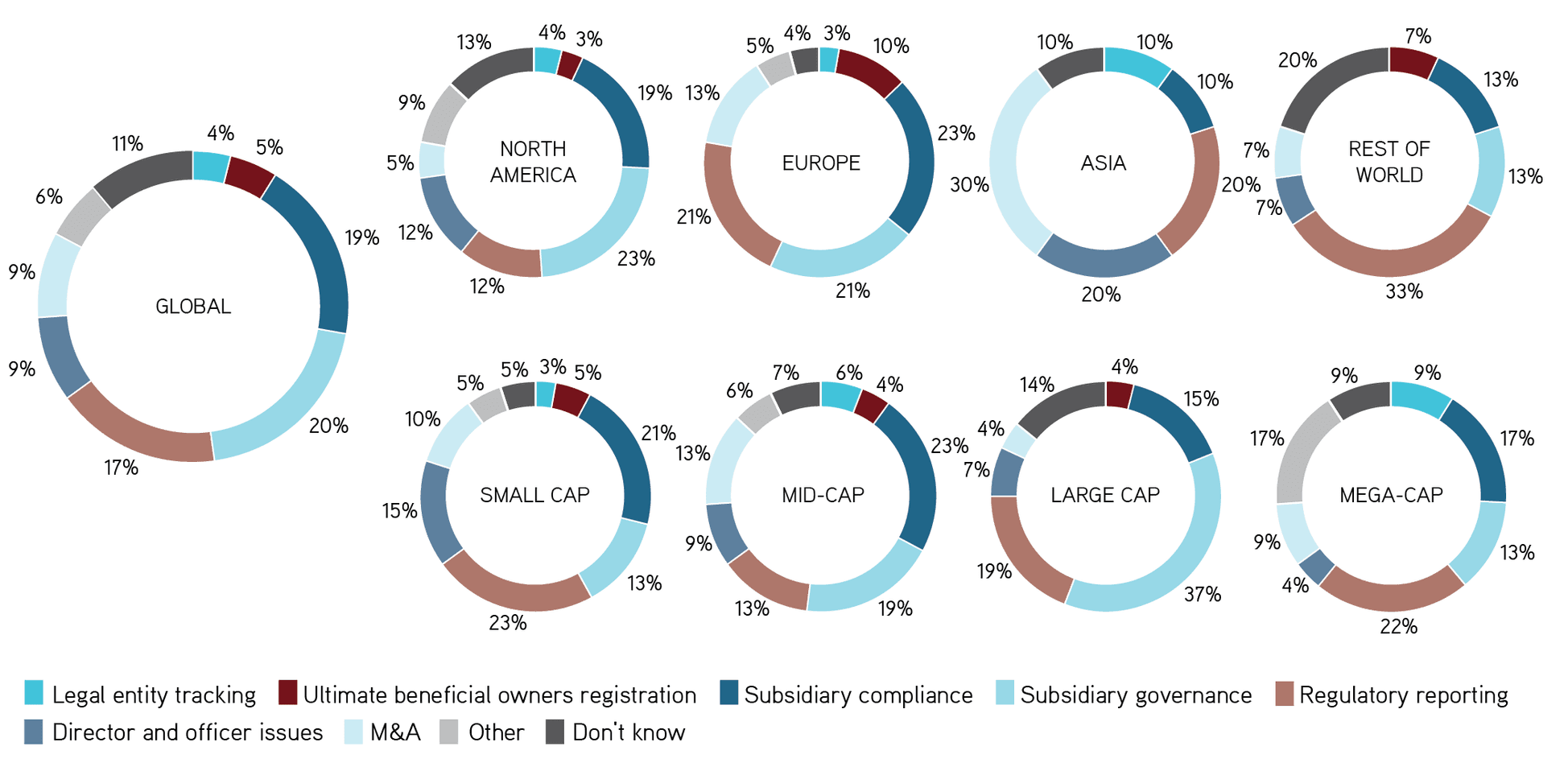

Subsidiary governance, mentioned by 20 percent of respondents, and subsidiary compliance, mentioned by 19 percent of respondents, lead the field in terms of entity management areas cited as taking up the most resources over the past 12 months. These are followed by regulatory reporting (17 percent), M&A and director and officer issues (9 percent each), ultimate beneficial owners registration (5 percent) and legal entity tracking (4 percent).

Director and officer issues are mentioned by 12 percent of those in North America but none in Europe, where 23 percent of respondents say subsidiary compliance took up the most resources over the last year. That compares with 19 percent of their peers in North America.

Similarly, one in 10 of those in Europe point to ultimate beneficial owners registration as using most resources, compared with just 3 percent in North America. Thirteen percent of respondents in Europe say M&A took up the most resources over the past year, while just 5 percent of those in North America say likewise.

In terms of company size, 37 percent of respondents at large-cap firms say subsidiary governance took up the most resources in the last year, compared with 19 percent of those at mid-cap companies and 13 percent each of those at mega-caps and small caps.

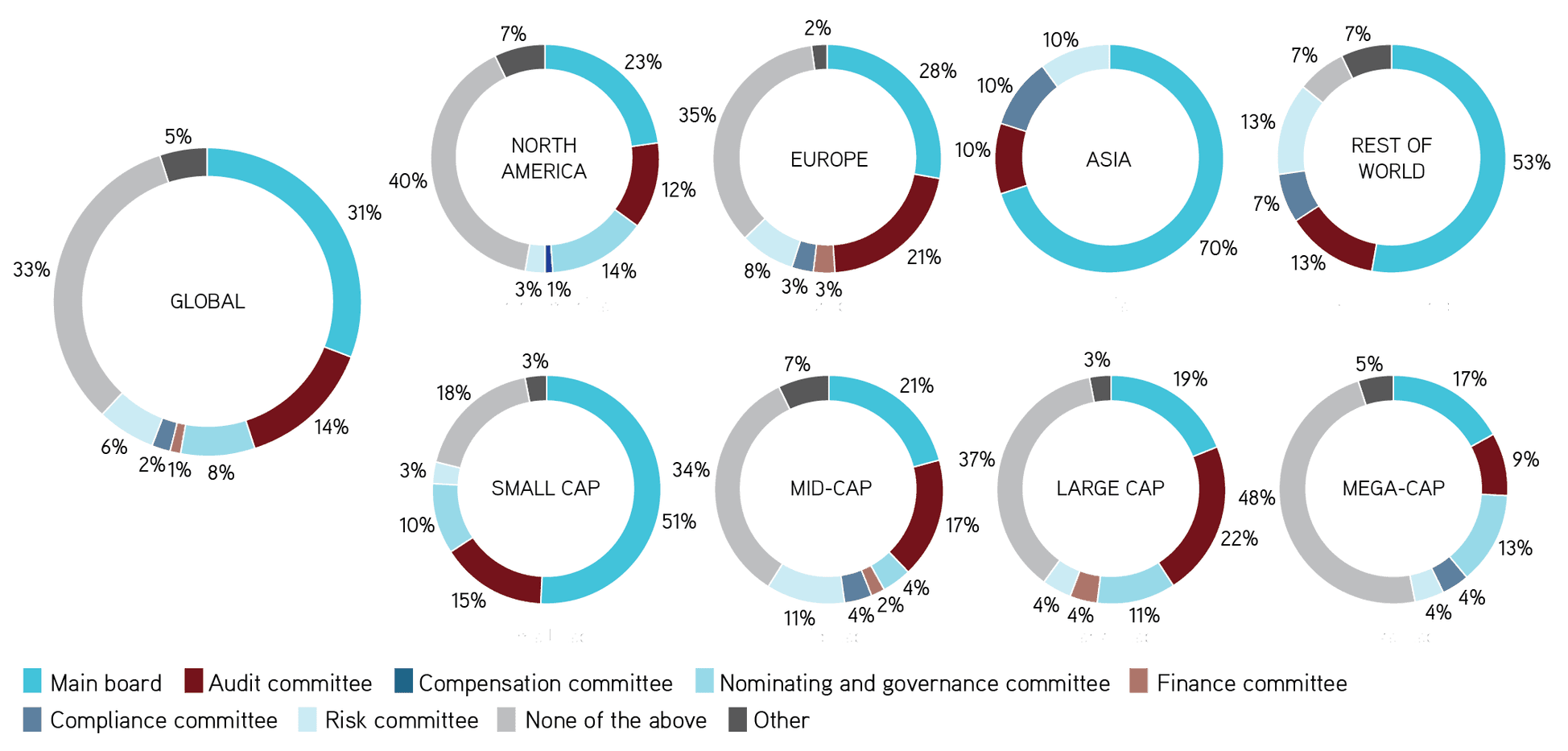

Entity management is conducted by management functions and outside advisers/service providers but, as in other areas, the board can play an oversight role. Overall, 31 percent of respondents say this role is primarily served by the main board, while 14 percent point to their audit committee. Others mention the nominating and governance committee (8 percent) or risk committee (6 percent). One third of respondents, however, indicate that neither the board nor any of its main committees has primary oversight of entity management.

This last response is particularly common among respondents at mega-caps (48 percent) and less so among those at small caps (18 percent). More than half (51 percent) of those at small-cap firms say their main board has primary oversight, compared with roughly one in five of those at other companies.

Regionally, 14 percent of respondents in North America say their board’s nominating and governance committee has primary oversight of entity management. None of those in Europe or Asia say likewise.

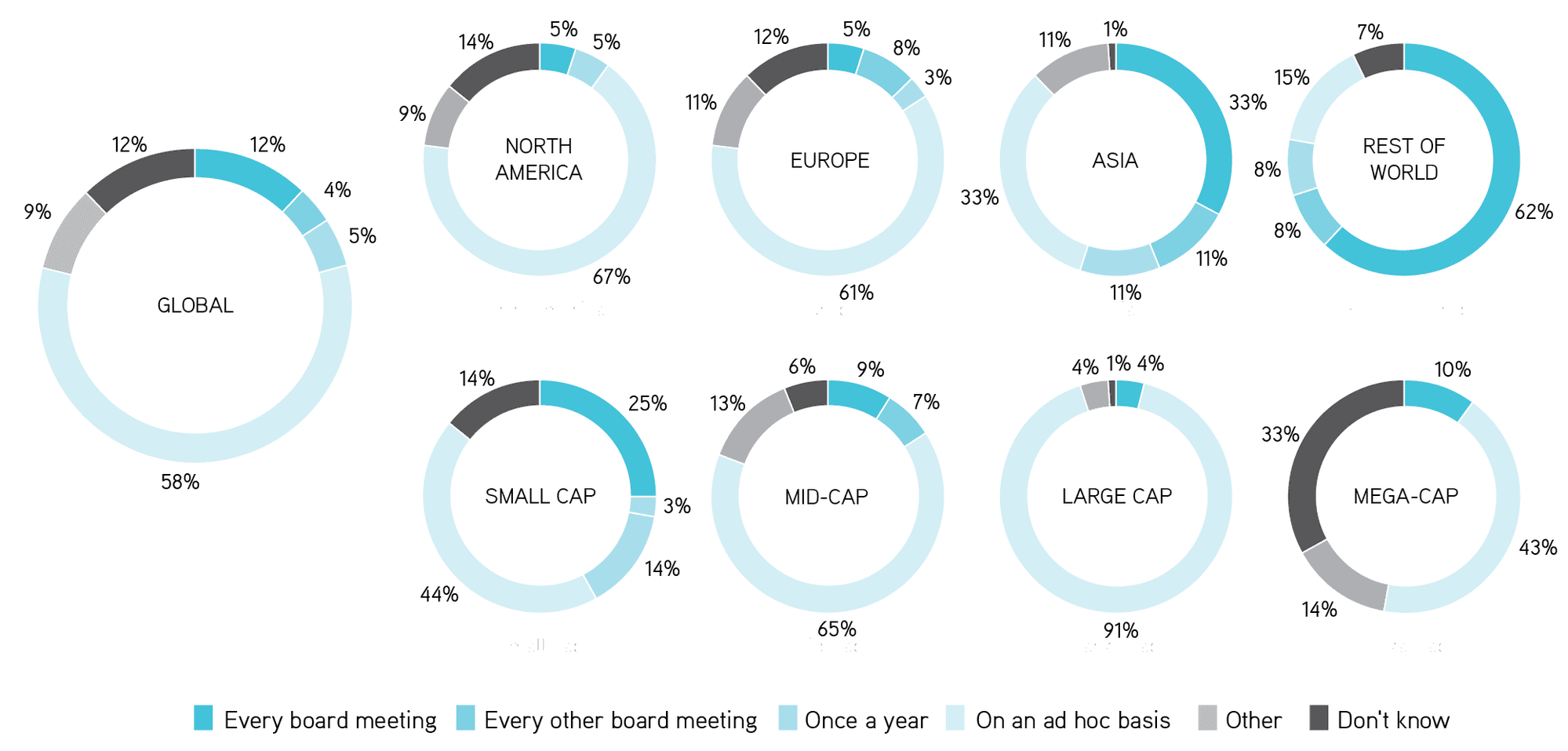

Overall, more than half (58 percent) of respondents say their main board discusses entity management issues on an ad hoc basis, while 12 percent say those discussions happen at every board meeting. Only a few say the frequency is every other meeting (4 percent) or once a year (5 percent).

More than nine in 10 large-cap respondents (91 percent) say their main board discusses entity management matters on an ad hoc basis, considerably more than those at mid-cap companies (65 percent) and more than twice as many as those at small caps (44 percent) and mega-cap companies (43 percent). A quarter of those at small-cap firms say these discussions happen at every board meeting, significantly more than those at mega-cap (10 percent), mid-cap (9 percent) or large-cap companies (4 percent).

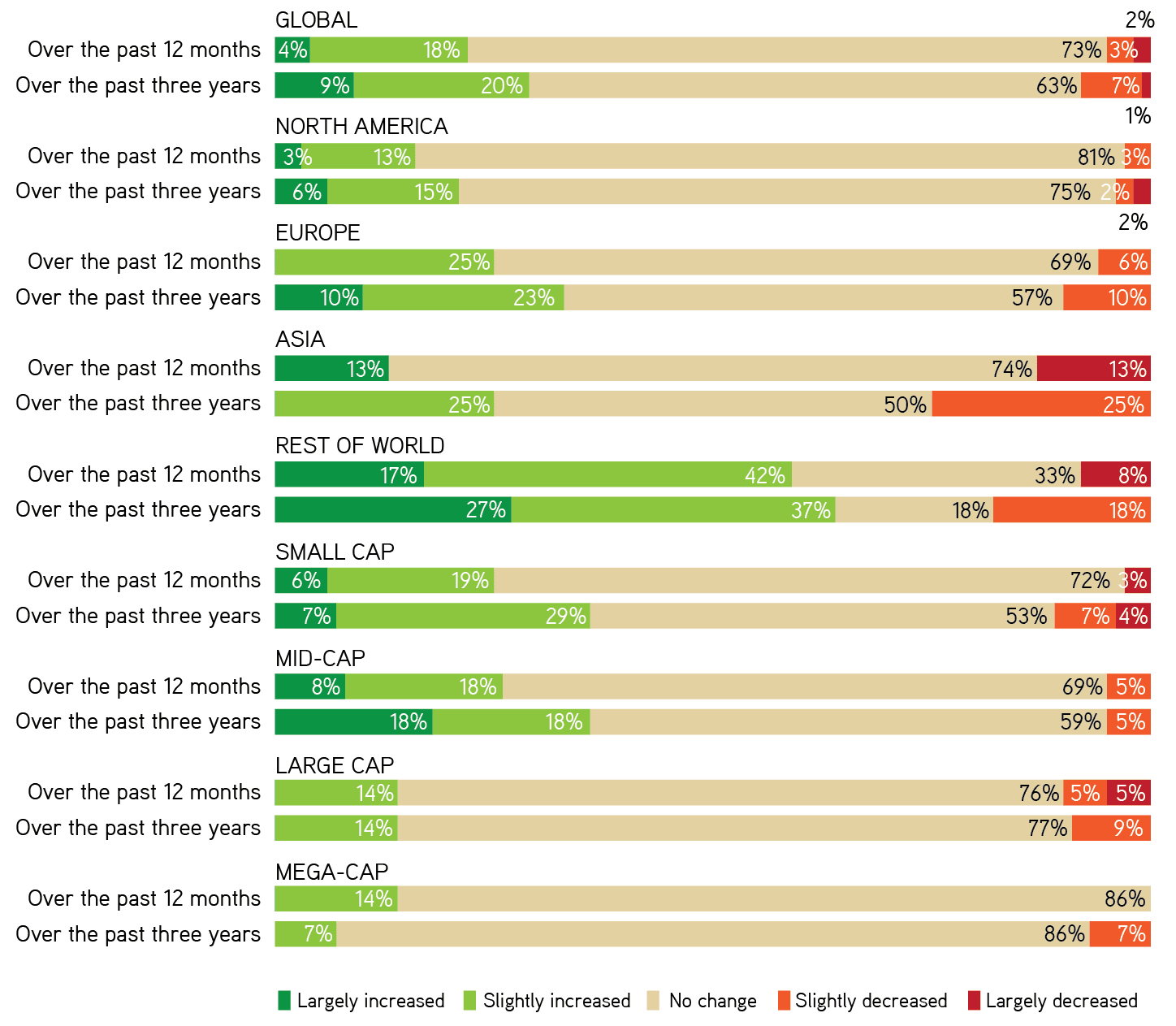

In almost three quarters (73 percent) of cases, respondents report that the frequency with which the board discusses entity management issues has remained stable over the past year. On balance, however, these discussions are taking place more often: 22 percent say there has been a slight or large increase in frequency compared with just 5 percent who say there has been a drop in frequency.

Looking back over the past three years, 29 percent of respondents say there has been a slight or large increase in the frequency with which their board discusses entity management, while 8 percent say there has been a decline in frequency.

Budget for entity management

Size of your entity management team

Use of technology for entity management

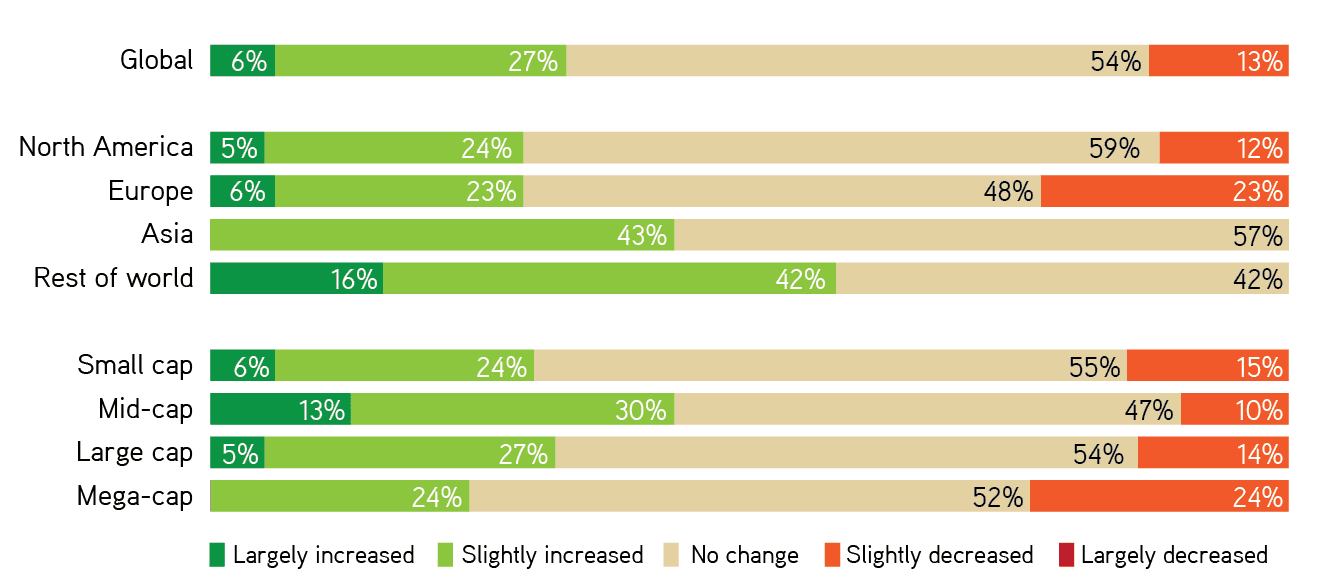

As noted earlier in this report, entity management demands a lot of resources and work conducted by both in-house and external advisers/service providers. Despite its core importance to companies, the function might be seen as at risk of declining funding during a time of economic uncertainty. Overall, however, one third of respondents report that their budget for entity management has experienced a slight or large increase over the past 12 months, compared with just 13 percent who say their budget has seen a slight decrease. Forty-three percent of respondents at mid-cap companies say their budget has grown over the last year.

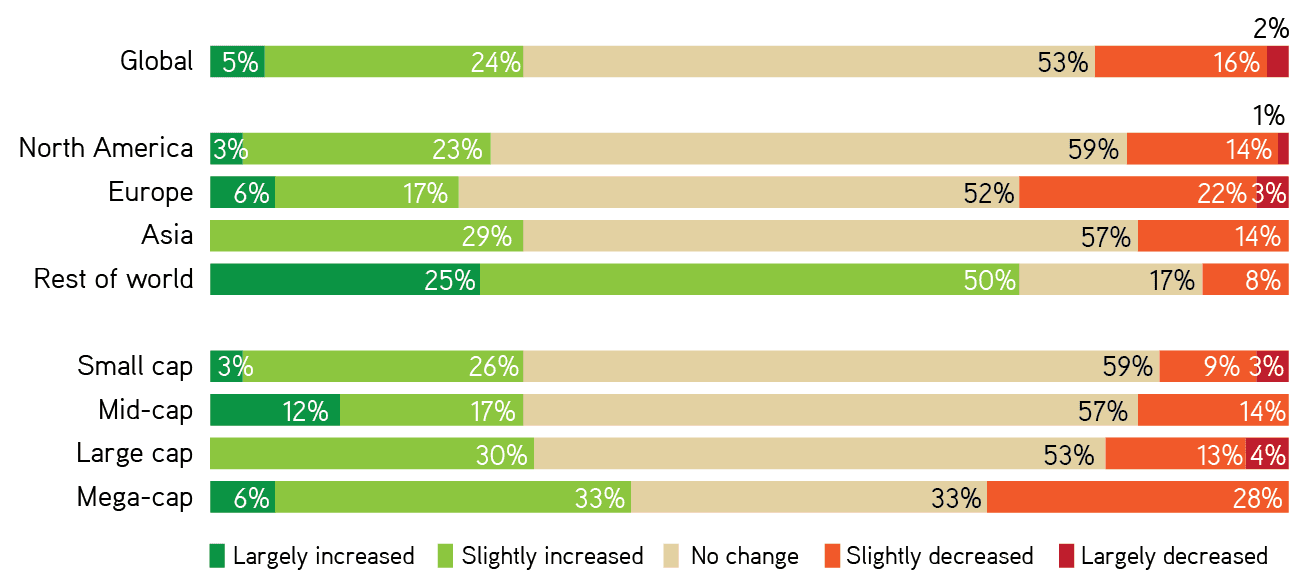

Similarly, 29 percent of respondents report that the size of their entity management team has increased over the last 12 months, while 18 percent say it has decreased.

Mega-caps appear to have experienced the greatest change, with 39 percent of respondents at those companies reporting a slight or large increase in the size of their team and 28 percent a slight decrease. Only a third of that group say their team has stayed the same size.

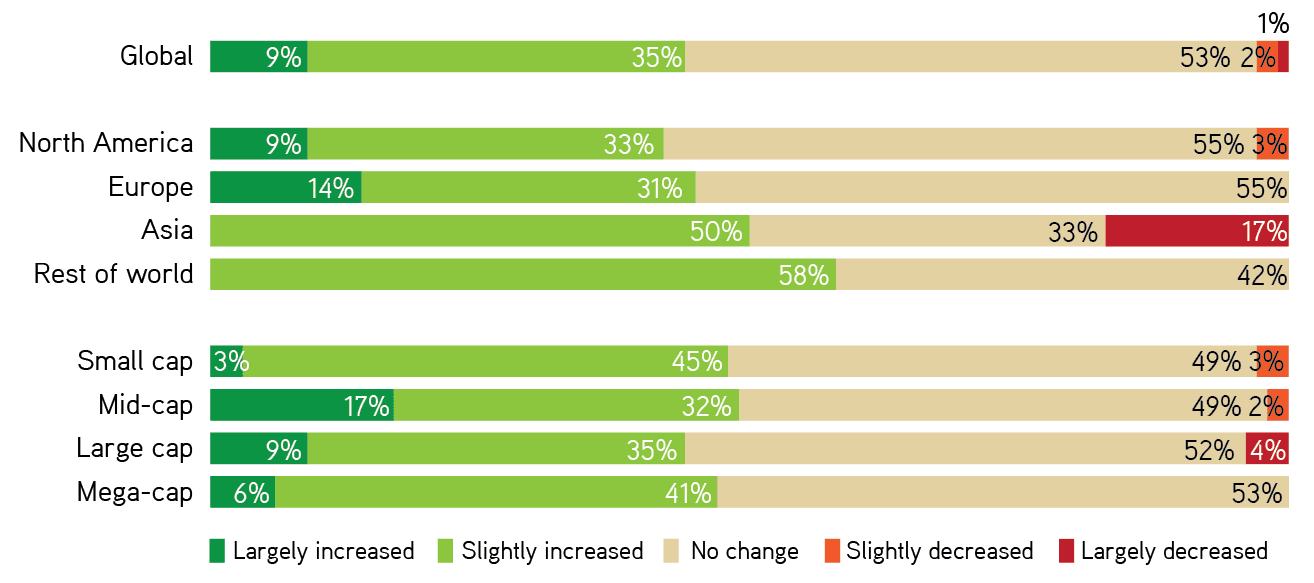

Aside from headcount, a key factor in the ability of entity management teams to be successful is their ability to deploy technology. Globally, 44 percent of respondents say their company has increased its use of technology for entity management over the last 12 months, with only 3 percent reporting a decline.

Those reported increases are broadly similar across different cap sizes, although it is notable that approaching a fifth (17 percent) of respondents at mid-caps say their company has seen a large increase in the use of technology in this field.

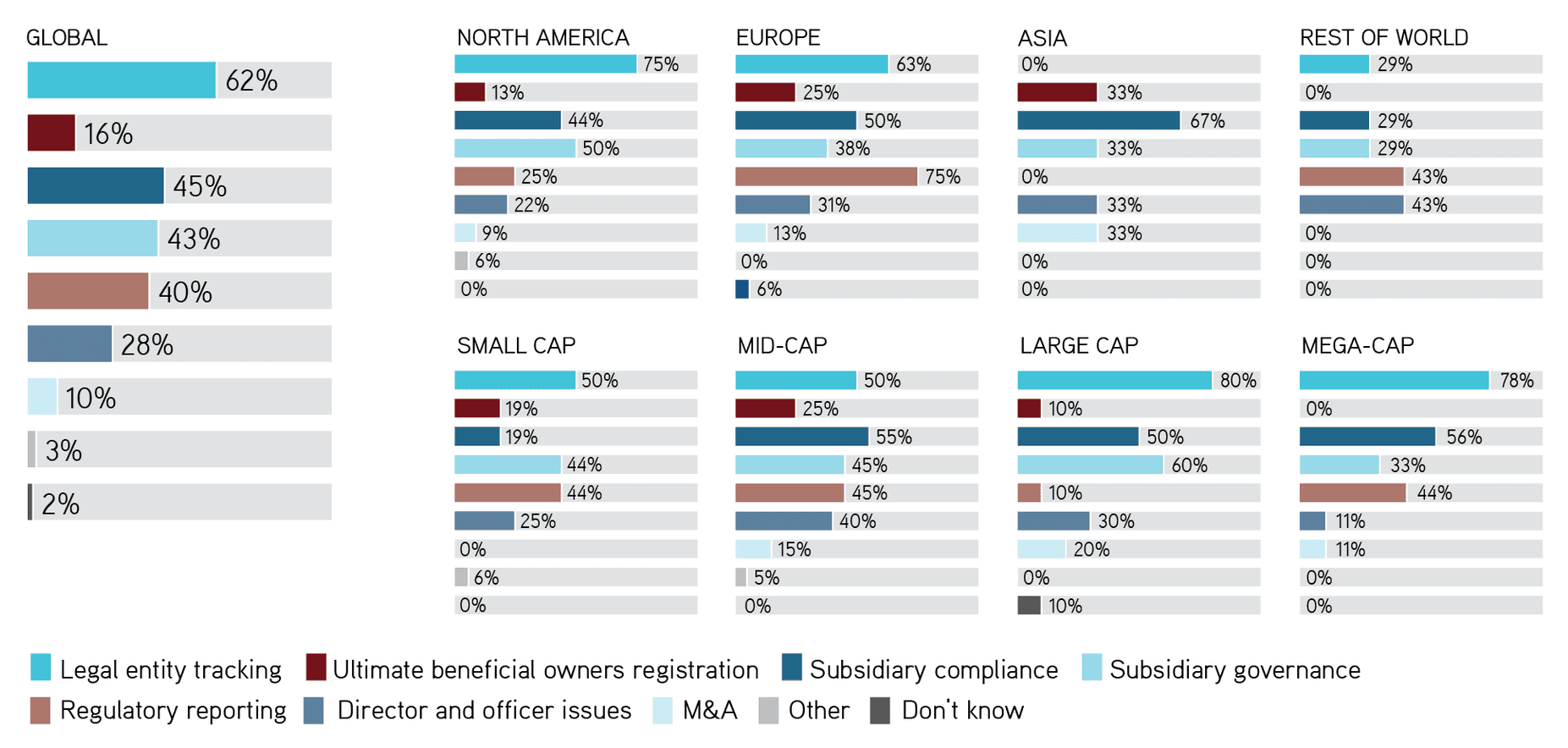

Among respondents who report an increased use of technology at their company in entity management, 62 percent say it is being used more widely for legal entity tracking.

This is followed by subsidiary compliance (cited by 45 percent of respondents), subsidiary governance (43 percent), regulatory reporting (40 percent), director and officer issues (28 percent), ultimate beneficial owners registration (16 percent) and M&A (10 percent).

The emphasis on using technology more extensively for legal entity management is most pronounced at bigger companies, with 80 percent of respondents at large caps and 78 percent of those at mega-caps saying they are making greater use of tech for this work, compared with just half of those at small caps and mid-caps.

Three quarters of respondents in Europe report making greater use of technology for regulatory reporting purposes, compared with just a quarter of those in North America.

The potential opportunities and risks of AI have become the center of attention in many areas, including corporate governance.

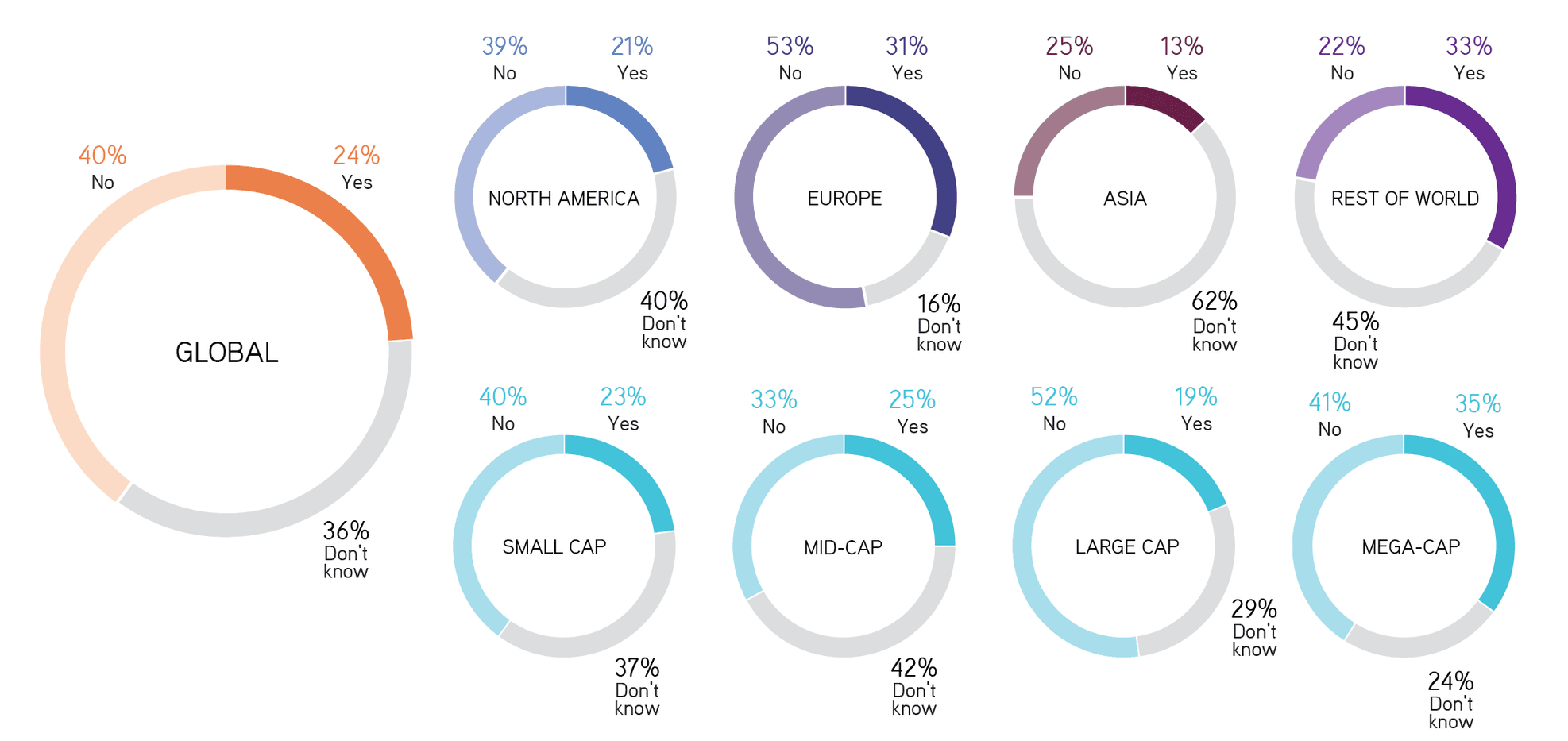

The situation is evolving rapidly but thus far the technology has not spread widely into entity management, according to respondents. Just 8 percent say their company is using AI as part of its entity management work. That figure is higher among those at mid-cap companies (11 percent) and small-cap firms (9 percent) than among those at mega-caps (5 percent) and large caps (4 percent).

More respondents in Europe (11 percent) report using AI than do those in North America (5 percent).

The study indicates that there will be a short-term uptick in the use of AI but also a large degree of uncertainty. Overall, 24 percent of respondents say their company’s in-house legal/governance function plans to start using AI over the coming year, while 40 percent have no such plans and more than a third (36 percent) don’t know.

Thirty-one percent of respondents in Europe plan to start using AI, but more than half (53 percent) say they don’t intend to, with just 16 percent not knowing. In comparison, 40 percent of those in North America don’t know whether their firm's in-house legal/governance function will move into AI, 21 percent say they will and 39 percent say they won’t.

Respondents at mega-cap companies are most likely to say their firm plans to start deploying AI for legal/governance work (35 percent). More than half (52 percent) of those at large caps say they have no plans to start using the technology.

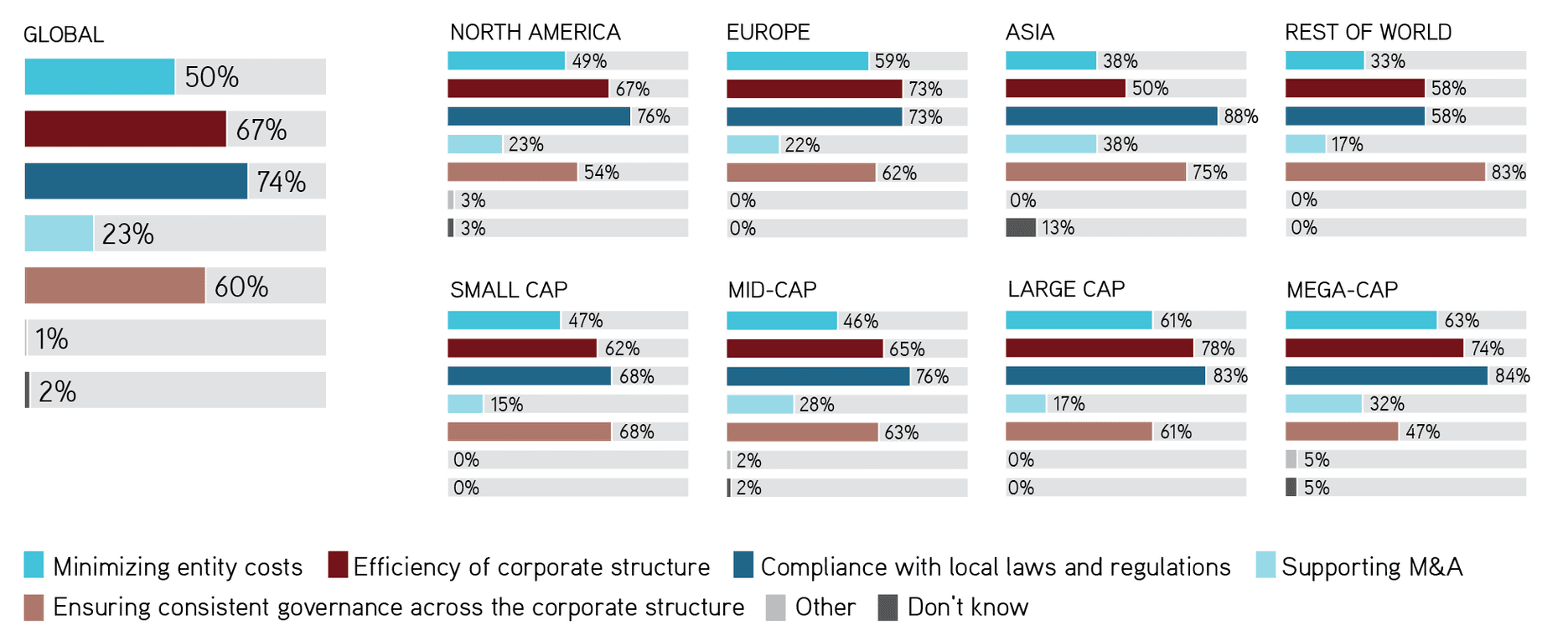

Complying with local laws and regulations is mentioned by almost three quarters (74 percent) of respondents globally as a priority for their company when it comes to entity management. That is followed by efficiency of corporate structure (cited by 67 percent of respondents), ensuring consistent governance across the corporate structure (60 percent), minimizing entity costs (50 percent) and supporting M&A (23 percent).

The focus on compliance is more prevalent among respondents at large caps (83 percent) and mega-caps (84 percent) than among those at small caps (68 percent) and mid-caps (76 percent). Similar patterns are evident in terms of minimizing entity costs and the efficiency of corporate structure.

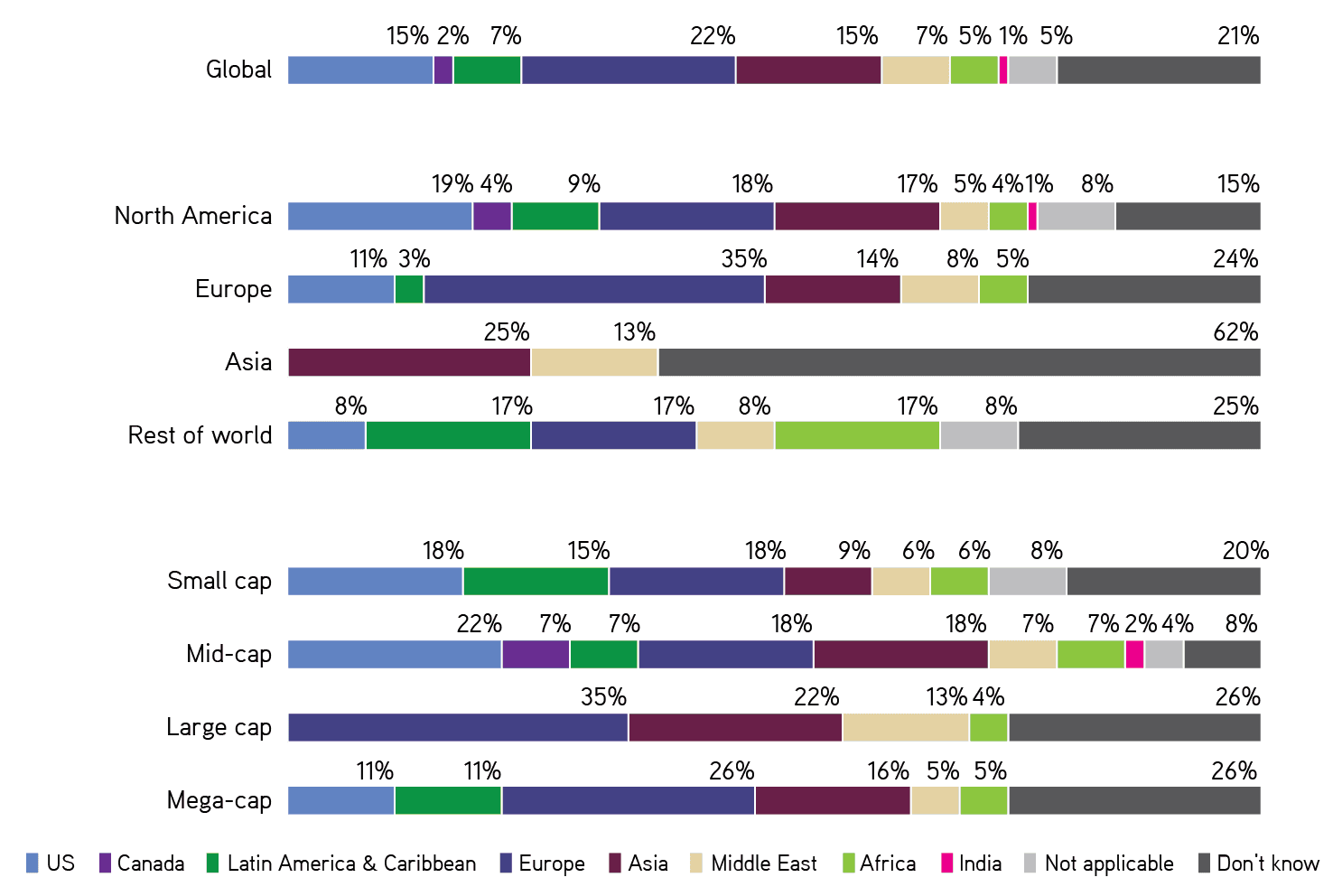

Overall, Europe (22 percent) is named most frequently as the region where conducting entity management is most difficult and/or expensive for respondents. The US and Asia place joint-second, each being mentioned by 15 percent of respondents.

Respondents also tend to find their home region challenging. The US rates as the most difficult and/or expensive for 19 percent of respondents in North America, with Europe cited by 18 percent and Asia by 17 percent.

Among respondents in Europe, 35 percent say Europe is the most difficult and/or expensive region for entity management, well ahead of Asia (14 percent) and the US (11 percent).

No respondents at large-cap companies say the US is the most difficult and/or expensive region, with 35 percent pointing to Europe, 22 percent to Asia and 13 percent the Middle East. By comparison, 22 percent of respondents at mid-cap companies say the US is the most difficult and/or expensive region in which to conduct entity management.

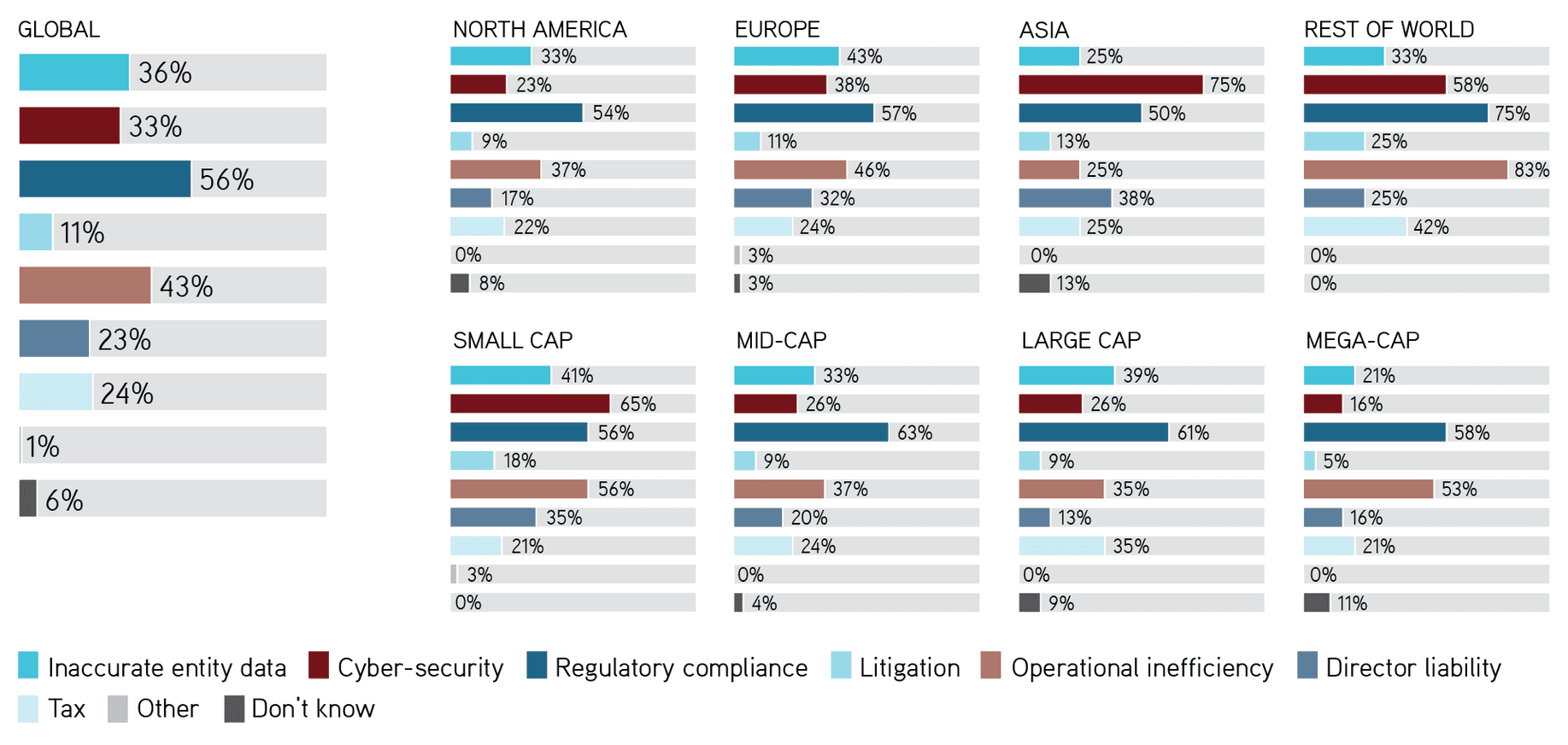

A key element of any entity management program is assessing risks. Among respondents globally, more than half (56 percent) say regulatory compliance ranks among the most important areas of risk their company faces in terms of entity management. This is followed by operational inefficiency (43 percent of respondents), inaccurate entity data (36 percent), cyber-security (33 percent), tax (24 percent), director liability (23 percent) and litigation (11 percent).

Forty-three percent of respondents in Europe see inaccurate entity data as most important, compared with 33 percent of those in North America. Similarly, 38 percent of respondents in Europe point to cyber-security as a main risk, while 23 percent of those in North America do similarly.

Cyber-security ranks among the top entity management risks for almost two thirds of respondents at small caps, compared with 16 percent of those at mega-caps and 26 percent each at mid-caps and large-cap firms. Similarly, director liability is seen as a major risk for 35 percent of those at small-cap companies, compared with 13 percent of those at large caps, 16 percent at mega-cap companies and 20 percent at mid-caps.

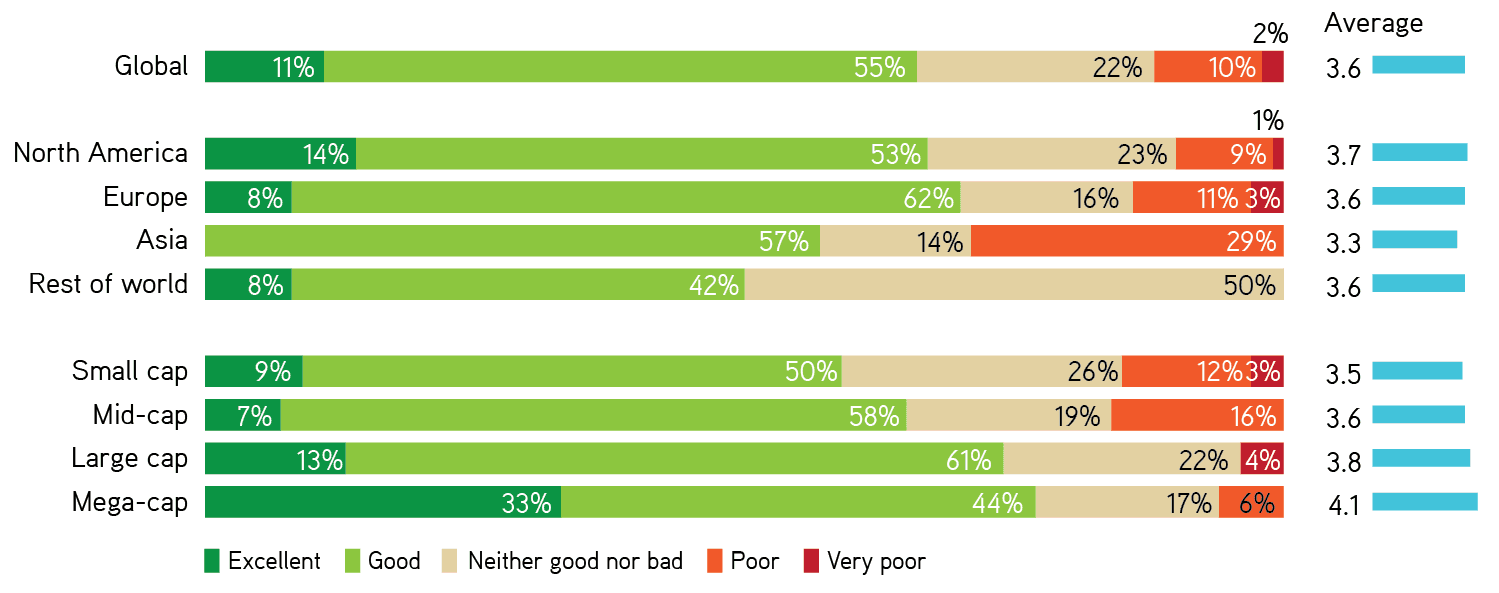

Overall, respondents have a positive view of their company’s entity management. They were asked to rate their program in terms of achieving its goals using a scale of one to five where one is ‘very poor’ and five is ‘excellent’. Globally, the average response is 3.6, with 55 percent rating their program as ‘good’ and 11 percent as ‘excellent’. Just 12 percent say their program is ‘poor’ or ‘very poor’.

Respondents’ rating of their entity management program improves, on average, at bigger companies. The average score among those at small caps is 3.5, increasing to 3.6 at mid-caps, 3.8 at large caps and 4.1 at mega-cap companies.

Regionally, respondents in North America have a marginally higher opinion of their entity management program (3.7) than do their peers in Europe (3.6).

Respondents were asked to name changes they would like to make to improve their company’s entity management program. Their comments include:

‘A budget to outsource entity management to a third-party service provider rather than relying on ad hoc internal resources and different local law firms around the world. A budget to streamline the group structure’

‘Better data management and analysis’

‘Better third parties on the ground’

‘Create awareness of its needs’

‘Develop more automation where possible – and where needed’

‘Digitalization. Increase management of IT and corporate use of AI for efficiency and cost savings’

‘Eliminate unnecessary entities’

‘Further automation and leveraging of technology, and overall simplification of legal entities’

‘Get the entity management service provider to make documents and reports more accessible’

‘Good data, especially with regard to integrity, and there must be an emphasis on cyber-security. Also, good use of technology and robust software. Another area of emphasis would be structure and architecture of reporting systems’

‘Greater efficiency, greater consistency and better planning’

‘Greater transparency and coherence across the whole structure’

‘Greater use of technology to create greater efficiencies’

‘Ask how AI can assist with improving shareholder engagement, conducting board self-evaluations, improving board efficiency and improving efficiency of regulatory reporting’

‘I would have a robust system to house it that is not overly expensive. We currently use a SharePoint site as we only have 40 or so entities. Platforms for this information are typically out of budget for us’

‘If we could find technology that could help us streamline and reduce workload on the team, that would be great’

‘Implementing a consistent and efficient approach to maintaining entities across all jurisdictions to reduce costs and time spent on routine entity activities’

‘Improve data accuracy and control’

‘Improved efficiency and accuracy of data’

‘Improved service providers’

‘Increased AI to ensure accuracy and speed’

‘Introduce greater consistency and efficiency. We hope to do this by streamlining the number of external providers to one per region’

‘Introduce technology to drive efficient and effective entity management programs’

‘Introduction of more widespread use of AI’

‘More budget to automate and digitalize with the use of more tools or more modules to existing tools’

‘More consciousness of this function and awareness of how it is executed in the company. Currently this is not quite disseminated’

‘More staff’

‘Process consistency, tracking matters, vendor and firm management and authorized signatory management’

‘Simplify the corporate organizational structure’

‘Simplify the structure of the holding companies up to the main parent company’

‘Software for management and maintenance of corporate records’

‘Use entity management system/software’

‘Use of one board portal for all entities’

‘Would like to have better data on markets we enter, especially tax and compliance constraints’