Governance Playbook

The way ahead for proxy statements

The proxy statement has come a long way in recent times. From text-only, black-and-white documents intended purely to meet SEC regulatory requirements, it has become an essential tool used to communicate with shareholders and beyond. Many now include imagery, graphics and new areas of disclosure that would have been unimaginable several years ago. Above all, they provide a much greater degree of transparency into their companies. That is good corporate governance.

‘I love the proxy,’ says Jim Polehna, corporate secretary and chief investor relations officer at Kelly Services. ‘I love the evolution of the proxy over the past few years. It’s been encouraging for investors.’

I love the evolution of the proxy over the past few years. It’s been encouraging for investors

In this special report we provide commentary from governance professionals at companies with leading-edge proxy statements on their work creating those documents. We also outline actionable steps and best practices for others as they seek to produce successful proxy statements that underline their corporate governance achievements. We look at why the proxy statement is important, how to get started each year, how to decide what to include, how to determine the best way to present information in non-textual ways, how to run an effective preparation process and how to determine whether your hard work has been a success.

Now more than ever it is important for the proxy statement to be an effective tool for your company.

When considering their proxy statements and all the work that goes into preparing them, companies need to establish why the document is important. This goes beyond merely complying with SEC requirements, although it is important to make sure nothing is missed from a regulatory perspective.

Rather, professionals say, the company – through its board, governance team and other corporate functions – needs to appreciate that the proxy statement is one of its key tools, along with the AGM, annual report and ESG report, for communicating with investors. This increasingly applies to other stakeholders such as employees.

‘It's the storybook [telling] what’s unique about a company,’ explains Kaley Childs Karaffa, head of board advisory for the Americas at Nasdaq.

She points out that, among other things, a growing number of retail investors are looking at proxy statements to help decide whether they want to buy a company’s stock – or even purchase its products.

‘I view it as our opportunity to communicate with our investors on corporate governance,’ says Mary Francis, corporate secretary and chief governance officer for Chevron Corporation. The company spends a lot of time talking to investors about finance and other matters, but governance is at the foundation, she adds.

Polehna describes the proxy statement as likely the document that gives the most valuable insight into companies, in part by providing an avenue to both explain their strategy and summarize their financial performance. He points out that the proxy statement can be useful in helping investors get to know management and the board of directors, provide insight on their interactions and explain how executive pay is tied to performance. Among other things, he points out, it can also be a tool for board recruitment.

Clear messagingJoseph Skrokov, senior director and assistant general counsel at Regeneron Pharmaceuticals, says his firm uses the proxy statement to provide clear messaging to shareholders about why its governance and executive compensation practices are as they are. This is particularly the case where those practices are outside the norm, such as in having a staggered board or board members with longer tenures.

It's the storybook [telling] what’s unique about a company

Michael Rouvina, assistant general counsel for corporate governance and securities at Lumen Technologies, notes the importance of being able to tell a consistent story about the firm across its proxy statement, Form 10K and ESG report.

Erika Moore, corporate secretary and deputy general counsel at Nasdaq, says the proxy statement is followed by an AGM at which investors vote on proposals, meaning that it is also an advocacy document that needs to take into account who those investors are and what they want.

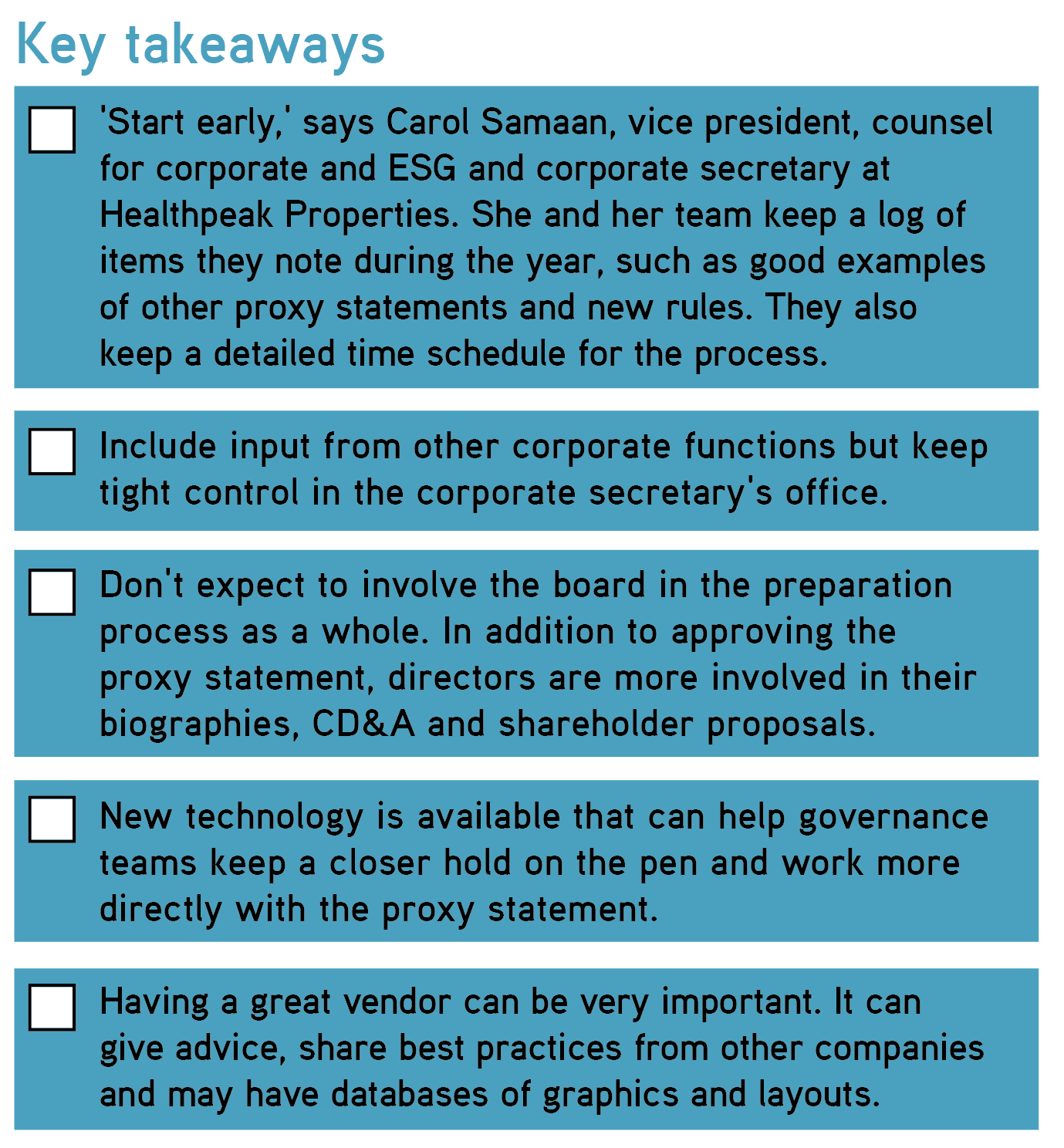

Before getting started with work on the proxy statement, governance professionals recommend taking time to assess the previous year’s document and decide what changes, if any, need to be made in terms of content and style. The corporate secretary should lead this review with input from directors, Karaffa says.

Feedback from investors and the company’s proxy statement vendor are all means to assess the direction of the next proxy statement. Governance professionals say other important components of conducting their review and planning for the next document include reviewing peers’ proxy statements – particularly those that win or are nominated for industry awards – and looking at proxy adviser and investor voting policies. This report will explore this process in more detail in the following sections.

The content of the proxy statement is set in part by traditional SEC requirements, which companies must ensure they comply with. Beyond that, however, governance professionals say it is increasingly important to understand what shareholders want to see disclosed. The key to that is engagement. ‘You can’t have a successful proxy statement if you don’t have a successful investor engagement program,’ Rouvina says.

In general, investor interest has in recent years led to many firms expanding their proxy disclosures regarding board oversight of risk – including ESG issues – board composition, board committee duties, director biographies, succession planning, CD&As, human capital management and diversity, equity & inclusion, among other things.

Company-specific issues can also arise from engagement. For example, governance teams may want to consider whether the board or the firm has made any changes, such as new governance practices, that need further explanation in the proxy statement, Moore says.

Francis notes that in Chevron’s 2023 proxy statement it wanted to draw a throughline about what the company is doing and how that pertains to the director nominees. With 2024 also being an election year in the US, companies may want to focus on political spending and lobbying activities, she adds.

Skrokov says one of Regeneron's investors thought it would be helpful to add a section to the proxy statement explaining the lead independent director’s duties.

Chris Weber, managing counsel for corporate, securities and governance at McDonald’s Corporation, says his company will continue to expand its ESG disclosures – in part because, given it is such a large business, it wants to demonstrate where those efforts have been focused. Among other things, in the last couple of years McDonald’s has also provided more detail on board refreshment in terms of both process and outcomes.

Engagement can also unearth existing or potential investor concerns that should be addressed in the proxy statement. For example, if shareholders want to see changes in board composition, the company could use the following year’s proxy statement to outline steps it is taking to refresh the board.

In other areas, a poor say-on-pay result should – as best practice – lead to significant levels of investor engagement. This engagement and any changes the company has made to its executive compensation practices should be explained in the following year’s proxy statement. A number of companies have in recent years enjoyed significant success in boosting their say-on-pay vote support levels by taking these steps.

Regulatory influences Governance teams should also keep an eye on changing SEC requirements. For example, as of last year companies must provide pay-versus-performance information in tabular form for the last five completed fiscal years.

This proved to be a time-consuming process in putting together 2023 proxy statements. With new disclosure requirements, many companies are seeking advice both from outside counsel and by looking at what peers are doing.

For 2024 proxy statements, companies should pay attention to the SEC’s new cyber-security disclosure rules. These require firms to provide information to investors and the market about material cyber-security incidents and the controls they have in place to protect against such attacks. At time of writing, it is also possible the SEC will finalize its long-awaited climate-change risk-disclosure rule in time for the 2024 proxy season.

Experts have a variety of views on how much disclosure relating to the cyber-security and climate-change rules should appear in the proxy statement versus a Form 10K or ESG report. For some, the issues they raise can be addressed by explaining board risk-oversight practices and structures. Rouvina suspects the SEC will want to see more disclosure in proxy statements about board-level skills and education, both in terms of cyber-security and more generally. Industry thinking on this topic will develop over the coming months.

Beyond rule changes, governance teams – perhaps via outside counsel – should also keep tabs on guidance the SEC provides through comment letters on specific companies’ reporting. For example, the agency has in the past asked for greater disclosure regarding boards’ risk oversight and the roles committees play.

Proxy advisers’ and major investors’ proxy voting guidelines are other sources of insight for what to include in the proxy statement, as is looking at peers’ documents. Ki Hoon Kim, associate general counsel at Hewlett Packard Enterprise (HPE), says such benchmarking is helpful but cautions that reviewing every element of peers’ proxy statements may not be a good use of time.

Rather, he tends to focus on areas such as board skills matrices and board biographies, particularly in light of the universal proxy. The CD&A section is also ripe for more regular benchmarking because there is a great deal of focus on it and because companies often use both in-house and external expertise to produce it, Kim notes.

You can’t have a successful proxy statement if you don’t have a successful investor engagement program

As proxy statement disclosures have expanded in recent years, so has the length of many documents – in some cases to more than 100 pages. This can raise cost issues and potentially overwhelm investors. One means to increase disclosures in a more condensed yet easily digestible manner is to use graphics, tables and imagery. Many companies and their vendors have successfully adapted to this dynamic.

One of the areas where there has been a marked uptick in the use of graphics is board skills and diversity matrices but they vary widely in how they are styled and the information they include. For example, some firms offer more aggregated diversity information in terms of gender, race/ethnicity and other metrics. This is an area where engagement with investors can determine whether they prefer more individualized information.

Governance professionals note that in some cases skills matrices give most directors credit for being experts in most fields. This reduces the value of the matrix as it leaves little differentiation between board members and suggests a low bar is applied to being deemed an ‘expert’. One solution is for governance teams to ask directors for more detailed information on their experience and skills in each area and to devise a scoring system that determines who qualifies as an expert. This can be a helpful alternative to relying on directors to self-select their areas of expertise.

Governance professionals note that the CD&A section is another area where graphics can be useful. Rouvina says that before the introduction of graphics to his CD&A, it ‘was like reading a novel’. The data involved can be highly detailed and may be less appropriately presented in text, particularly for retail investors. Charts and graphs are also helpful in CD&A sections where there are comparisons between individuals at the company, between pay and targets, between peer companies or between pay and certain metrics, which increasingly include ESG targets.

Another area where experts say graphics can be of use to investors is in an introductory section giving an overview of the company’s financial performance, strategy, values and products. Experts also say there is value in other non-traditional layouts such as Q&As with directors or photographs of the board.

Strike a balanceAlthough graphics and other design can be very helpful, professionals say they can be overused to the extent they become confusing and overwhelming for readers. A balance needs to be struck.

There are several different ways to achieve this. For example, Skrokov says he and his team will sometimes spend a great deal of time working on a new graphic – only to drop it at the last minute in favor of bullet points. Sometimes a graphic can try to say too much, he explains.

‘If you’re going to use a graphic, it has to emphasize a point or tell a story in a more compelling way,’ Karaffa says.

Other design elements to consider include online navigability such as an interactive table of contents. It is also important to consider the overall flow of the document so that it is logical to readers. In addition, Henrique Canarim, senior assistant general counsel at Leidos, says his firm has tried to harmonize the design of its proxy statements with its other branding by including cross-functional input.

If you’re going to use a graphic, it has to emphasize a point or tell a story in a more compelling way

Several corporate functions will be involved in preparing the proxy statement to varying degrees, including finance, HR, legal, compensation, audit, sustainability, investor relations and the board. Law firms, design firms, printers, proxy solicitors and executive compensation advisers will also likely play roles.

But the process must be led by the corporate secretary’s team and, in the words of governance professionals, that team must keep a ‘close hold of the pen’ when it comes to drafting the document. Among other benefits, this avoids having ‘too many cooks in the kitchen’. The best practice outlined by experts is for the corporate secretary’s team to produce an initial draft before getting feedback from board committees, compensation consultants, outside counsel and key management groups, among others, and finally seeking approval from the board.

The board is not typically deeply involved in the preparation of the proxy statement. Kim says that in November, his team gives the HPE board a preview of the company’s AGM, including plans for the proxy statement and any shareholder proposals, but does not send the board drafts as the process goes along.

Governance professionals say the board typically has most input on members’ biographies and that the compensation committee or its chair will be involved in finalizing the CD&A section.

Specific board committees may also be involved in board responses to shareholder proposals that feature in the proxy statement. Members of the board will be involved if the proxy statement features Q&As with them, too.

Technological tools can play an important part in the proxy statement preparation process.

Some governance teams send Word files to the outside firm putting the document together. In what has been described as an important shift, others have started using cloud-based platforms that enable them to enter and edit text in a stylized document that looks much like the proxy statement itself.

Ultimately, governance teams – and their boards and companies – want to know whether their proxy statement has been a success. Among other things, that will help inform their approach to the following year’s document. Shareholder engagement can be an important means of getting feedback. It can reveal any investor criticisms of the current proxy statement or their wishes for next year’s version of the document.

On the other hand, ‘if they don’t say anything, that’s usually a sign [the proxy statement] is fulfilling its purpose,’ Kim says.

Karaffa says companies can measure the success of the proxy statement by seeking out how it resonates not only with investors, but also with employees, suppliers and other corporate stakeholders.

Experts note that there aren’t many strict methods for measuring success. But some say one of the best metrics to look for is the degree of support the company receives in voting at its AGM, particularly on director and executive compensation proposals. Weber notes that McDonald’s typically faces multiple shareholder proposals and will look at the level of support those receive – particularly in relation to support for similar proposals at other companies.

Proxy advisers’ feedback and voting recommendations are a further indicator of how effective the proxy statement’s disclosures are, although they also relate to business or governance practices at issue with a shareholder proposal.

As noted previously, experts will pay close attention to whether their work is nominated for or wins industry awards as well.

Does the proxy statement include an opening letter from the CEO with substantive information about the company, its story, its performance and its plans?

Does it also include a substantive letter from the board or lead independent director?

Does the document include a proxy summary that clearly outlines and sets the tone for the document, including elements such as corporate performance and images of the product(s) the company sells?

Does the proxy statement provide detailed information about board members, their skills and experience, their diversity and why they should be directors at the company?

Is there extensive information about the role of the board, its process and practices, and about committees and their work, particularly with respect to risk oversight, including cyber-security and ESG?

Is the CD&A section written in understandable language?

Does the proxy statement disclose the company’s shareholder engagement efforts and any changes it has made as a response to investor feedback?

Does the document have a logical flow?

Does it make effective use of graphics, tables and other design elements, particularly in board matrices and the CD&A section?

Does it comply with all necessary SEC regulations?