By Erin Connors, Mark Olsen, Rob Peters and Miriam Robin

This summer, we asked hundreds of individuals working for and with public companies about a topic of increasing concern: the reporting of information relating to their company’s ESG efforts.

We surveyed a broad spectrum of individuals, including compliance professionals, members of the C-suite and professional advisers like accountants, lawyers and IR professionals. We asked a broad spectrum of companies, across a broad spectrum of industries, with a broad spectrum of market caps and a broad spectrum of workforce sizes. And we received a broad spectrum of answers.

Indeed, the one theme that recurs in answers to our questions regarding the ESG reporting process is a lack of certainty. To an extent, that may be healthy. Respondents take a variety of approaches to reporting issues, and over time that may help the market discover best practices for ESG reporting organically.

But survey respondents also express a different and more troubling kind of uncertainty: a lack of knowledge about important ESG issues. They do not know how costs affect their firm's ESG commitment, they do not know whether ESG-related information should appear in their financial reports and they do not know whether their own company’s ESG reporting is accurate.

Their answers may express uncertainty but, from that uncertainty, a clear message emerges: the market is begging for direction on ESG reporting. Most respondents say their employer acts with good motives on ESG issues, and yet far fewer indicate that their ESG reporting can be trusted. Closing that gap will take guidance, if not mandates, from the SEC on how ESG reporting should be conducted. If and when it comes, it will likely be welcomed.

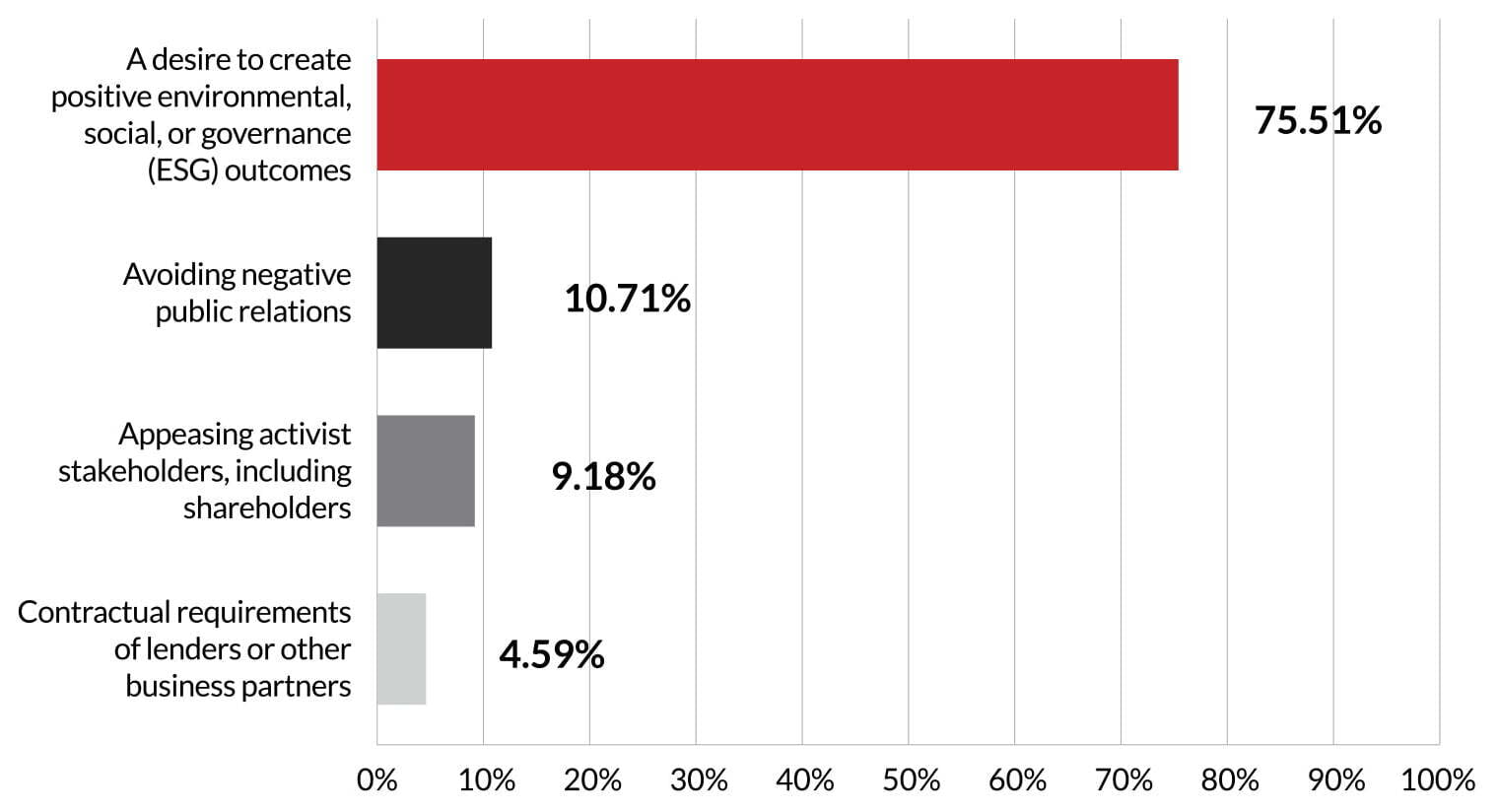

Commitment to ESG By a substantial margin, most survey respondents indicate that their company undertakes ESG initiatives primarily based on a pure desire to create positive outcomes. By contrast, only a quarter of respondents feel their employers are driven by external factors, such as a desire to avoid negative publicity.

Dissenting voices: Commentary from survey participants reveals – sometimes starkly – that an earnest belief in ESG causes is not shared by all. One respondent calls ESG ‘an inane ‘woke’ concept to be ignored’

Additional data from the survey, however, could be interpreted as uncertainty about the depth of corporations’ commitment to ESG initiatives – particularly when it takes dollars out of the company treasury. More than half of respondents (51 percent), for instance, acknowledge that they lack insight into the extent to which costs impact their companies’ level of commitment to ESG initiatives.

Likewise, only a small minority of employers (12 percent) tie their executive compensation to ESG goals. The low number here, of course, may reflect factors other than a lack of commitment. It may be, for example, that companies are struggling to identify ESG goals to shoot for, and how to translate them into compensation incentives.

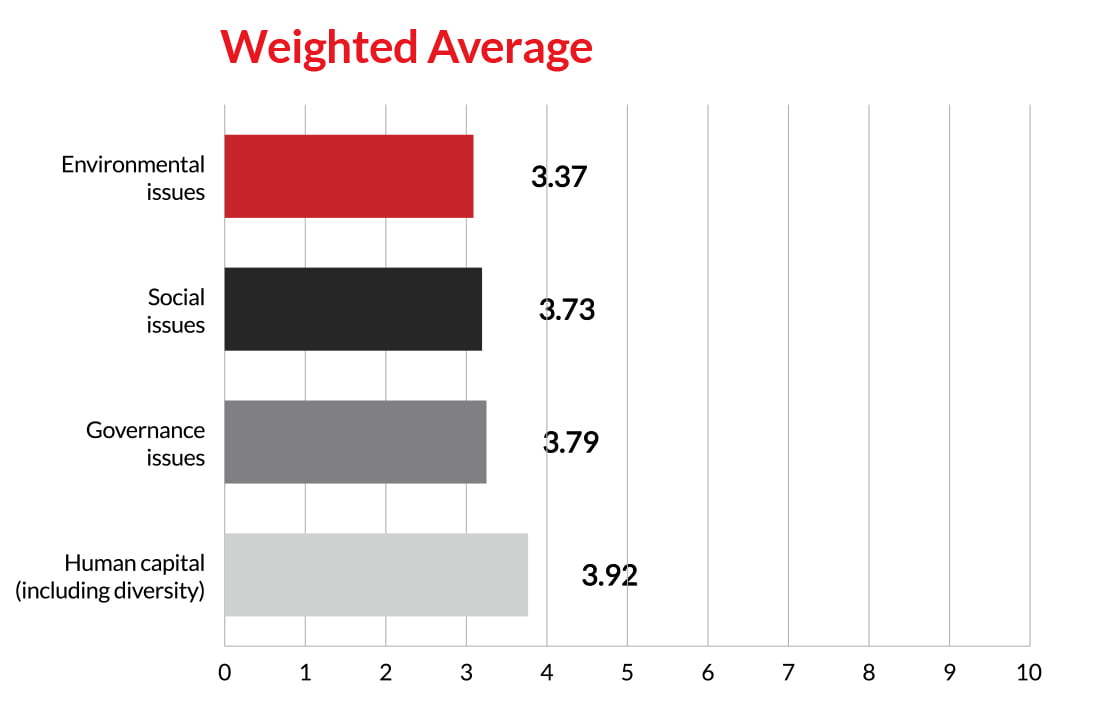

Of the three topics covered by ESG – environmental, social and governance matters – responses suggest that companies are least focused on environmental issues. Meanwhile, if human capital issues are separated out from the ‘social’ category, they receive the most attention of all.

ESG reporting process The lack of a regulatory framework for ESG disclosure (outside of the general obligation to disclose material information, at least) is most apparent in responses to our questions about ESG reporting.

The ‘all over the map’ quality of responses we received about ESG reporting is reflected in our question about the format companies use. Respondents are evenly split among three different formats, with 37 percent using an integrated sustainability/CSR annual report, 34 percent opting to integrate it into their public financial reporting and 29 percent issuing a regular ESG report separate from their public financial reporting.

Dissenting voices: Several comments from survey respondents indicate that their companies make ESG disclosures in multiple formats or are planning to expand their reporting in future years. Some, however, indicate that their company does no ESG reporting. ‘Since it’s not required, we don’t disclose anything meaningful,’ says one respondent

On the question of whether financial reporting should contain ESG disclosure, a plurality of respondents (42 percent) agree, albeit with a large undecided contingent (27 percent).

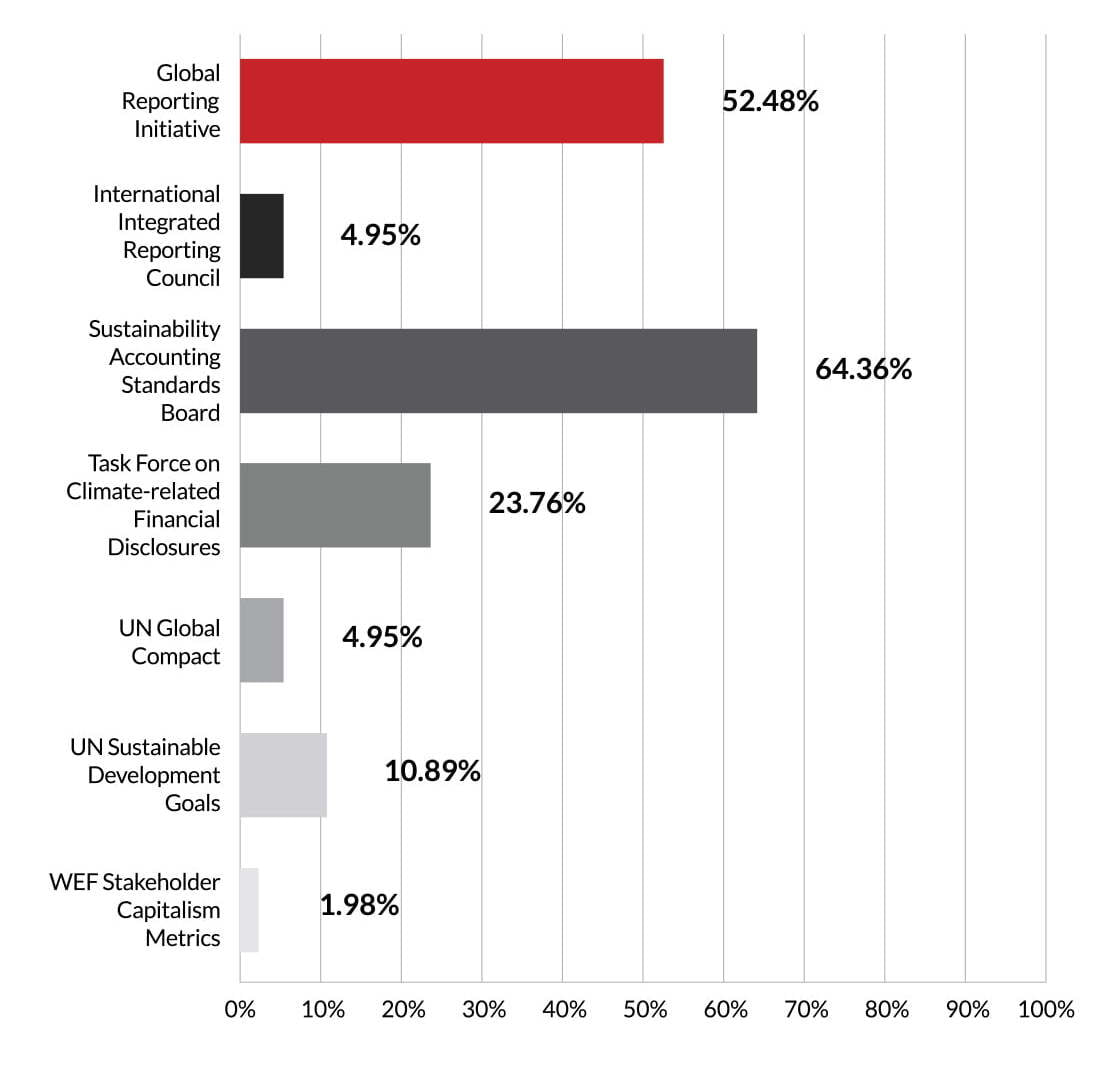

In the absence of clear disclosure mandates, companies are looking to multiple sources for guidance in drafting their ESG reporting. Those sources include their peers and multiple ESG frameworks by non-government standard-setting bodies.

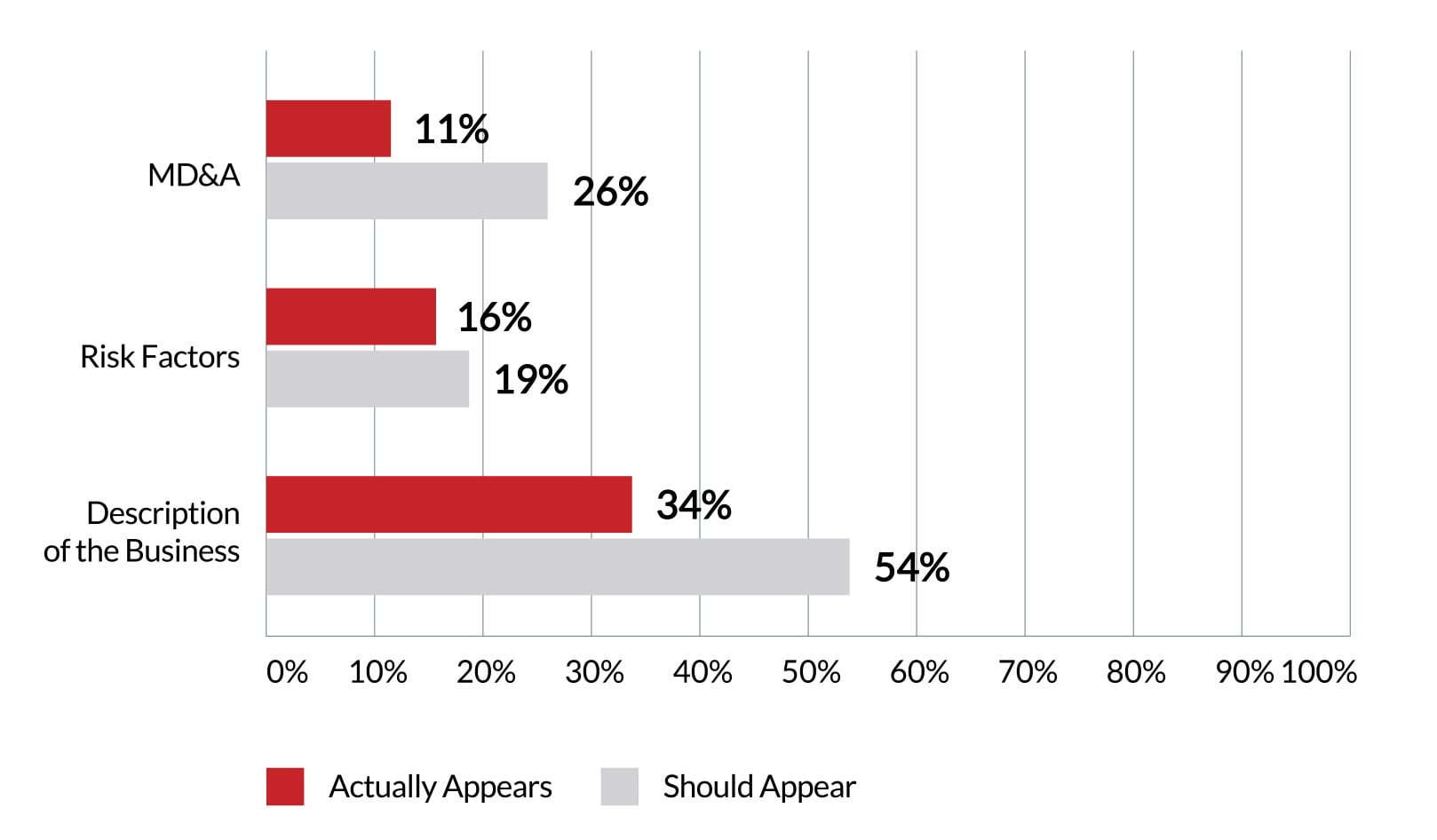

ESG reporting substance As with many topics relating to ESG disclosures, our respondents lack a strong consensus on where they do – or should – appear in public filings. By a slim margin, more respondents (55 percent) indicate that their ESG reporting appears in proxy materials as opposed to 10K filings. That narrow edge could be attributable to the intensity of investor interest in ESG issues.

For companies that do report through their 10Ks, responses reveal a gulf between which sections within the 10K form their reporting actually appears, and in which sections respondents think it should appear.

Dissenting voices: Several respondents say ESG information should not appear on the 10K anywhere. ‘It should be outside the 10K,’ says one. Others say the SEC should develop a separate section on the 10K dedicated to ESG reporting

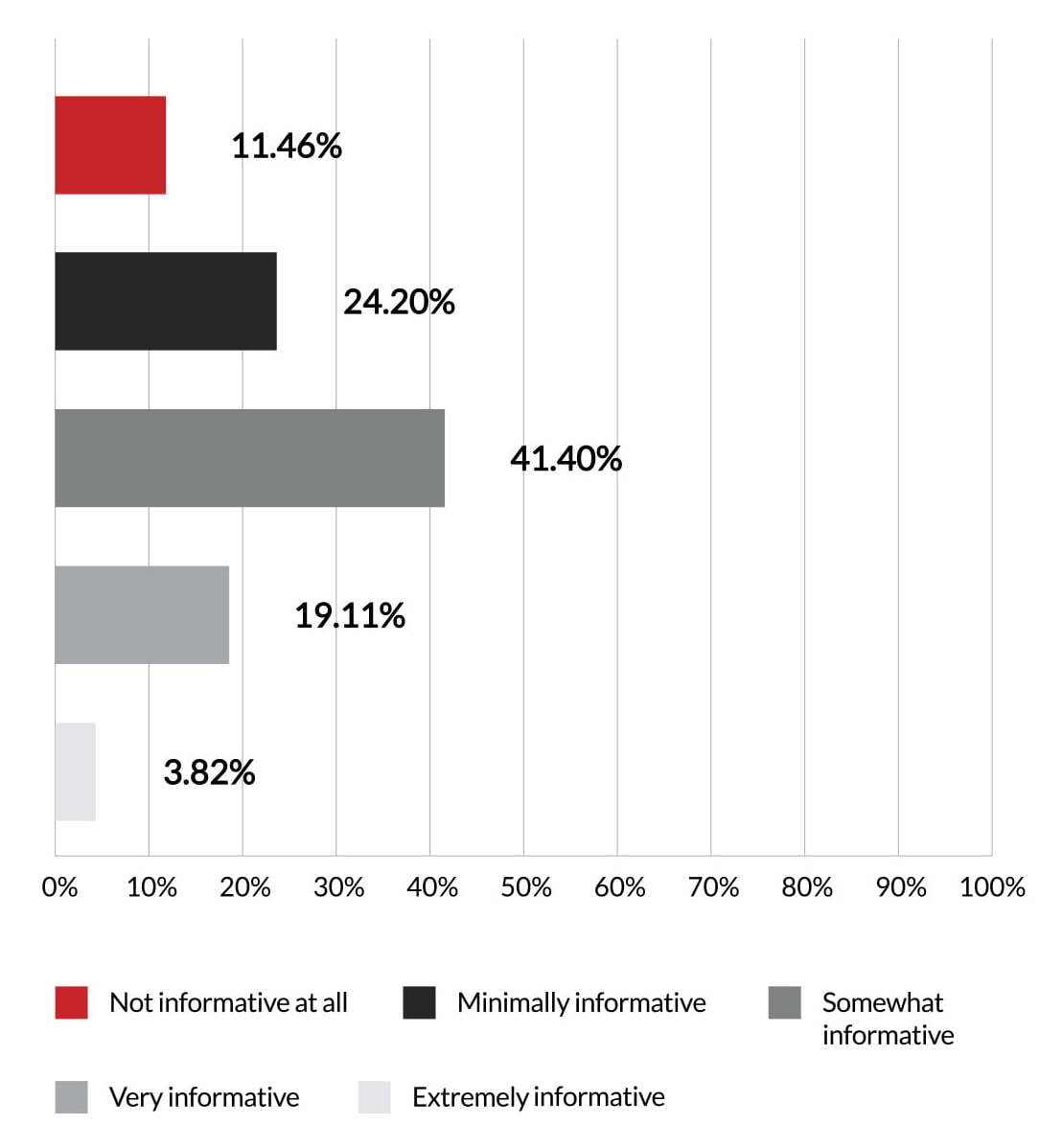

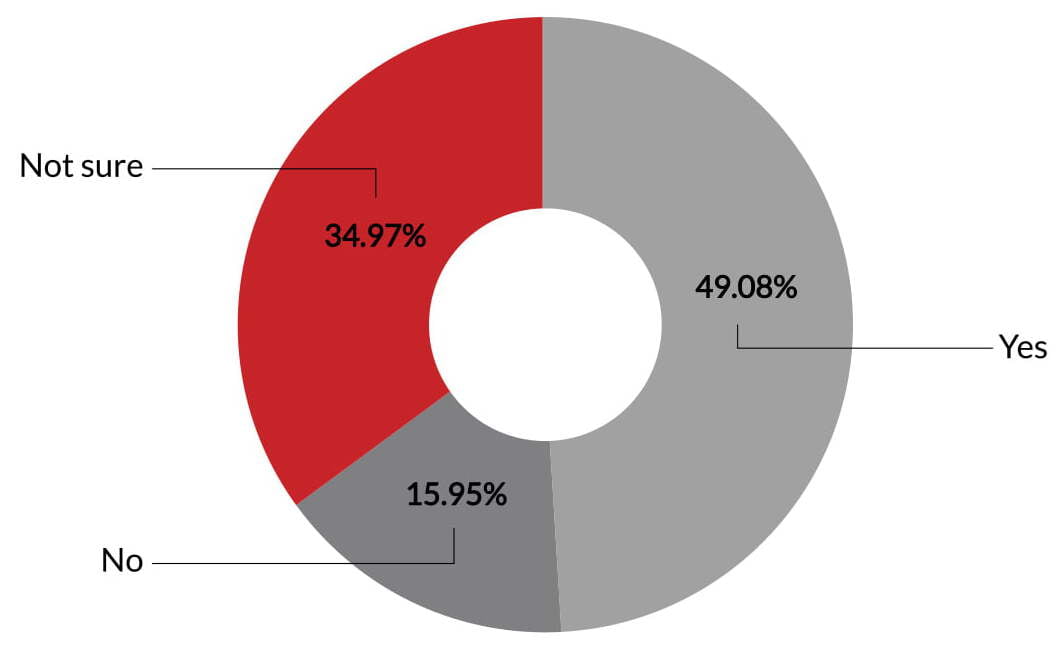

In two final telling data points, echoing the theme of uncertainty running through this report, respondents offer their views on how informative and accurate they find their company’s ESG reporting.

Viewed from one angle, the numbers offer reason for optimism. More than 60 percent of respondents believe their company’s ESG reporting is at least somewhat informative, and about half feel it is accurate. Even if neither number matches the 75 percent who believe their company is pursuing ESG initiatives from a desire to do good, it suggests that even in its present state, ESG reporting is offering some value.

Viewed from another angle, however, one number stands out: the 35 percent who cannot speak to the accuracy of their own company’s ESG reporting. It suggests, as does the whole survey, that there is considerable room for greater clarity on ESG disclosures – and, indeed, that many would invite greater clarity being imposed on them through SEC regulations. The question now is whether and when the SEC will take up that invitation.

Methodology Intelligize surveyed public company respondents and the accounting and legal professionals who advise them on their companies’ ESG activities. All responses were aggregated, and respondents were not asked to provide any personally identifiable information as part of the survey.

Responses came from companies across 14 different industries and 15 different job functions, ranging from CEO, CFO, attorney and accountant to reporting manager, controller and IRO, among others. While a near majority of respondents (46 percent) represent small-cap companies (under $2 bn), mid-caps and large caps are also well represented, at 31 percent and 23 percent, respectively.

Thirty-eight percent of respondents are from firms with fewer than 1,000 employees, while 34 percent employ between 1,000 and 5,000. Respondents with between 5,000 and 20,000 employees make up 14 percent of the sample size, with another 14 percent totaling more than 20,000 employees.

LexisNexis Legal & Professional® is a leading global provider of legal, regulatory and business information and analytics that helps customers increase productivity, improve decision-making and outcomes, and advance the rule of law around the world. As a digital pioneer, the company was the first to bring legal and business information online with its Lexis® and Nexis® services. LexisNexis Legal & Professional®, which serves customers in more than 160 countries and has 10,400 employees worldwide, is part of RELX, a global provider of information-based analytics and decision tools for professional and business customers.

Intelligize is the leading provider of best-in-class content, exclusive news collections, regulatory insights and powerful analytical tools for SEC compliance, transactional and IR professionals. Intelligize offers a web-based research platform that ensures law firms, accounting firms, corporations and other organizations stay compliant with government regulations, build stronger deals and agreements, and deliver value to their shareholders and clients.

Headquartered in New York City, Intelligize serves Fortune 500 companies, including Starbucks, IBM, Microsoft, Verizon and Walmart, as well as many of the top global law and accounting firms. In 2016, Intelligize became a wholly owned subsidiary of LexisNexis.

For more information, visit www.intelligize.com.