By Neil McCarthy, senior director at Morrow Sodali

The SEC has just completed its oversight role for the 2022/2023 season over challenges brought by companies to exclude proposals submitted by their shareholders per Rule 14a-8. What follows is a summary of the results for this season with comparisons to the 2021/2022 season.

Under Rule 14a-8, companies generally must include shareholder proposals in their proxy statements to be considered at the annual meeting. The rule, however, provides several bases for exclusion, including 13 substantive requirements that proposals must comply with to avoid exclusion – Rule 14a-8(i)(1) to (i)(13) – as well as procedural requirements for when and how they must be submitted to the companies by shareholders. The rule has a process for how companies can seek to exclude these proposals by submitting a challenge to the SEC to obtain a favorable ‘no-action letter’.

Challenges down 24 percent from 2021/2022 and submitted proposals outpacing last seasonWe saw 184 challenges this season compared with 241 last season, a decrease of 24 percent. So far this season, 635 shareholder proposals have been included in annual proxy statements, compared with 573 for all of last season. If the 2023 season-end total reaches 700, as we expect, that would be a 22 percent increase.

Given that the number of submitted proposals is up, but the number of challenges is down, we point to the SEC’s adoption of staff legal bulletin (SLB) 14L to help explain why.

SLB 14L (November 3, 2021)

Rescinded staff legal bulletins 14I, 14J and 14K.

Refocused the Rule 14a-8(i)(7) ‘ordinary business’ exception for proposals, raising significant social policy issues on the policy issue, rather than impact on the company.

Board analysis is no longer expected. The micromanagement exception was curtailed.

Economic relevance exception made inapplicable for proposals that raise issues of broad social or ethical concern related to the firm's business.

The effect of SLB 14L has made it more difficult to challenge many proposals, particularly for those related to environmental and social issues. It can be found here.

Observations (season over season)

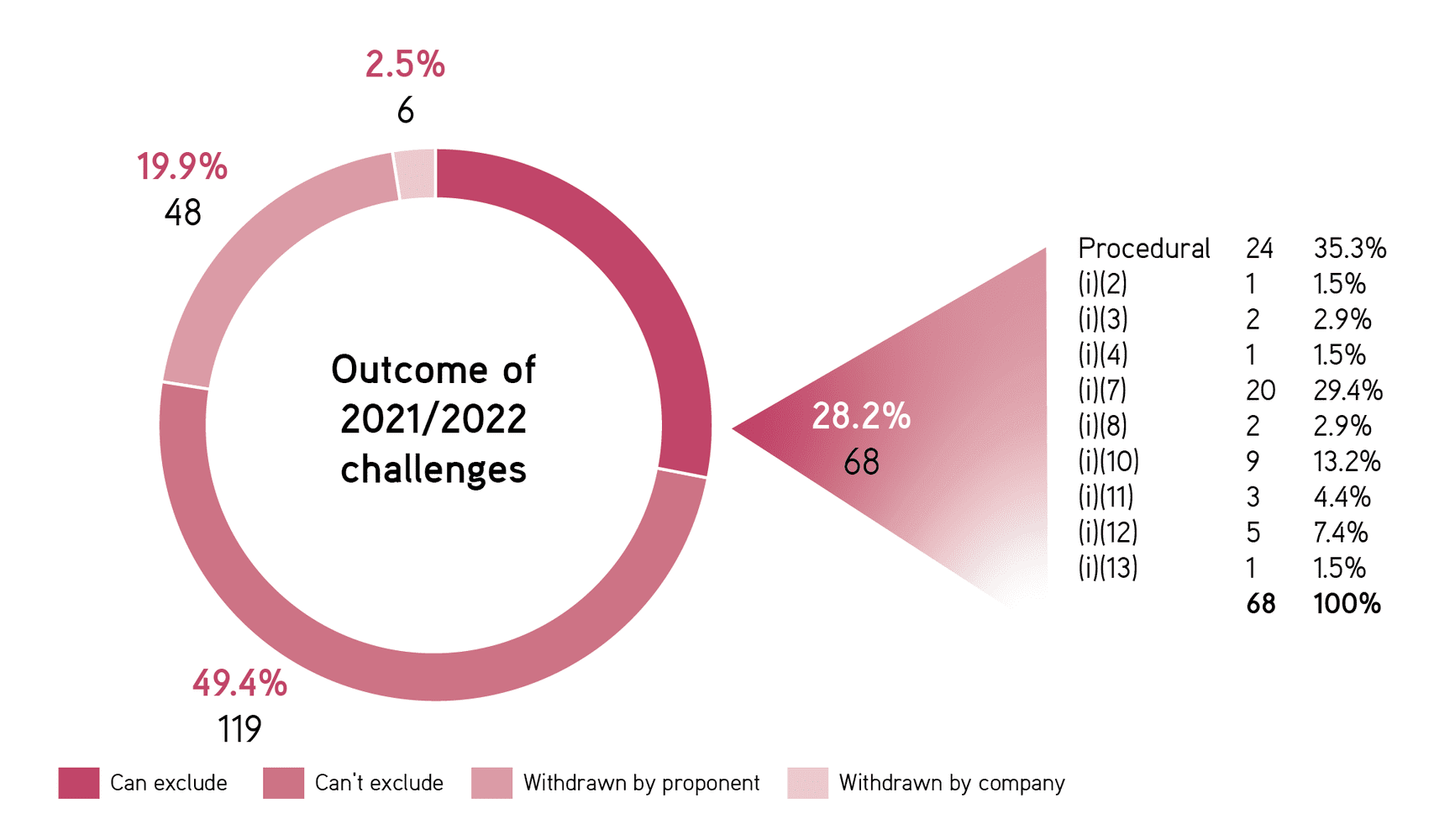

Challenges were down year over year by 24 percent from 241 to 184.

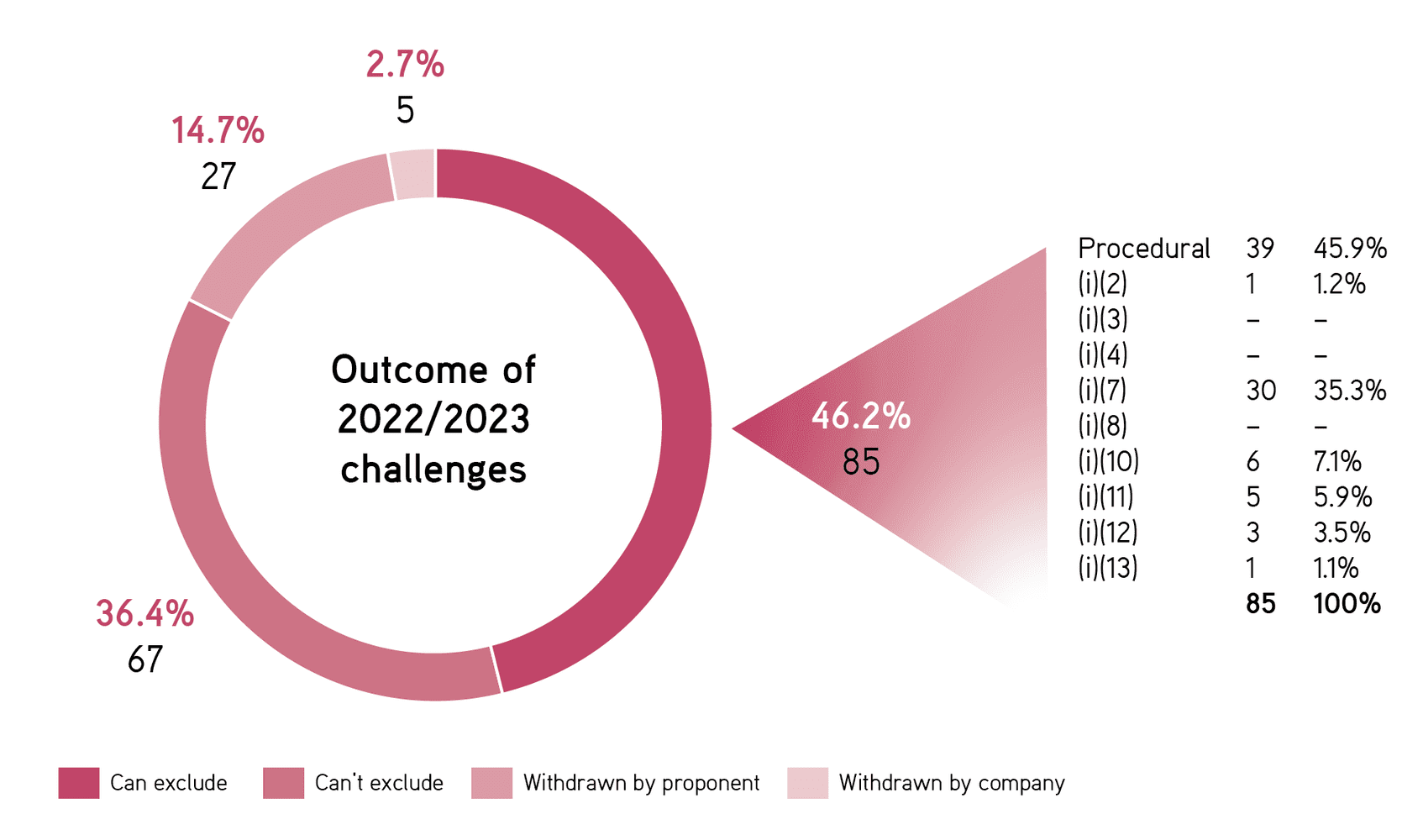

For those proposals that were challenged this season, the SEC allowed exclusions at a higher rate (46 percent vs 28 percent) and a greater number (85 vs 68) than it allowed last season.

Procedural exclusions were up, both as a percentage of all exclusions (46 percent vs 35 percent) and in absolute number (39 vs 24).

Exclusions under 14a-8(i)(7) ‘ordinary business’ were up as a percentage of all exclusions (35 percent vs 29 percent) and in absolute number (30 vs 20).

Percentage of proposals withdrawn was in line with 2021/2022.

Given the adoption of SLB 14L, we expected an increase in procedural challenges, and many were successful. We were initially surprised by points two and four above, and attribute it to a change in the mix of proposals submitted, especially for novel proposals on environmental and social issues. We plan to explore this further as we continue to track proposals that have been included in annual proxy statements, and the voting results, with our weekly reports.

Requests for reconsideration

The National Center for Public Policy Research (NCPPR) was denied reversal of SEC rulings for AT&T and JPMorgan Chase. In both cases, NCPPR requested a commission review but was denied; the staff reaffirmed its initial ruling, which relied on Rule 14a-8(i)(7) to find that the proposal ‘did not transcend ordinary business matters’.

The AT&T proposal sought a ‘report on the potential risks and consequences to the company associated with the prioritization of non-pecuniary factors when it comes to establishing, rejecting or failing to continue network relationships on its DirecTV platform.’

The JPMorgan Chase proposal sought a ‘report on the risks created by company business practices that prioritize non-pecuniary factors when it comes to establishing, rejecting or failing to continue client relationships.’

In both cases, NCPPR made similar arguments for reconsideration, including 17-page and 18-page assertions of ‘viewpoint discrimination by the staff under the First Amendment of the United States Constitution, arbitrary and capricious agency action, action in excess of the commission’s statutory authority under the Exchange Act, and incorrect application of Rule 14a-8(i)(7) by the staff.’

We note in this context that NCPPR is known for submitting ‘anti-ESG’ proposals that typically get low voting support. On April 28, 2023, NCPPR sued the SEC in the Fifth Circuit over its 14a-8 practices, a case we will be following with interest.

As You Sow/Green Century Funds were denied reconsideration over a proposal submitted to Amazon.com that sought disclosure of Scope 3 greenhouse gas emissions from its full value chain, as 99 percent of the company’s sales are for third-party products. The staff had relied on Rule 14a-8(i)(7) for exclusion as ‘the proposal seeks to micromanage the company by imposing a specific method for implementing a complex policy disclosure without affording discretion to management.’

Proposed SEC rulemakingOn July 13, 2022, the SEC proposed to amend three of the substantive grounds for exclusion:

Rule 14a-8(i)(10): Substantial implementation

Rule 14a-8(i)(11): Duplication

Rule 14a-8(i)(12): Resubmission.

For full details, please see SEC Proposal Release 34-95267 and the SEC Fact Sheet on the proposed rules. If adopted, we can expect an increase in the inclusion of shareholder proposals that would have otherwise been excluded under the prior staff interpretation of these provisions.

Morrow Sodali has been tracking 14a-8 developments with two weekly reports. One tracks proposals that have been included in annual proxy statements and the voting results. For this season, we’ll continue this coverage for annual meetings through June 2023, with a season-end summary in July 2023.

The other, which this paper summarizes, tracks challenges to inclusion brought by companies per Rule 14a-8. If you’d like to receive these free reports, please contact Jennifer Carberry.

Procedural grounds for exclusion are set forth in Rule 14a-8(b)-(f) and include failure to submit the proposal by the required date and failure to adequately prove ownership of shares that are beneficially held in ‘street names’.

In two cases this season, the SEC ruled sua sponte for exclusion on the basis of Rule 14a-8(i)(7). In one case, the company had relied on 14a-8(i)(10); in the other, the company had relied on a procedural argument with Rule 14a-8(f)(1).

Morrow Sodali is a global corporate consultancy that provides clients with comprehensive advice and services relating to corporate governance, proxy solicitation, M&A, activism, ESG, capital markets intelligence, shareholder and bondholder engagement and contested situations, financial communications, investor relations and research.

From headquarters in New York and London, Morrow Sodali serves more than 1,000 corporate clients in 80+ countries, including many of the world’s largest multinational corporations. In addition to listed and private companies, its clients include financial institutions, mutual funds, ETFs, stock exchanges and membership associations.

Contact:

Jennifer Carberry, senior director of marketing

+1 203 658 9419j.carberry@morrowsodali.com