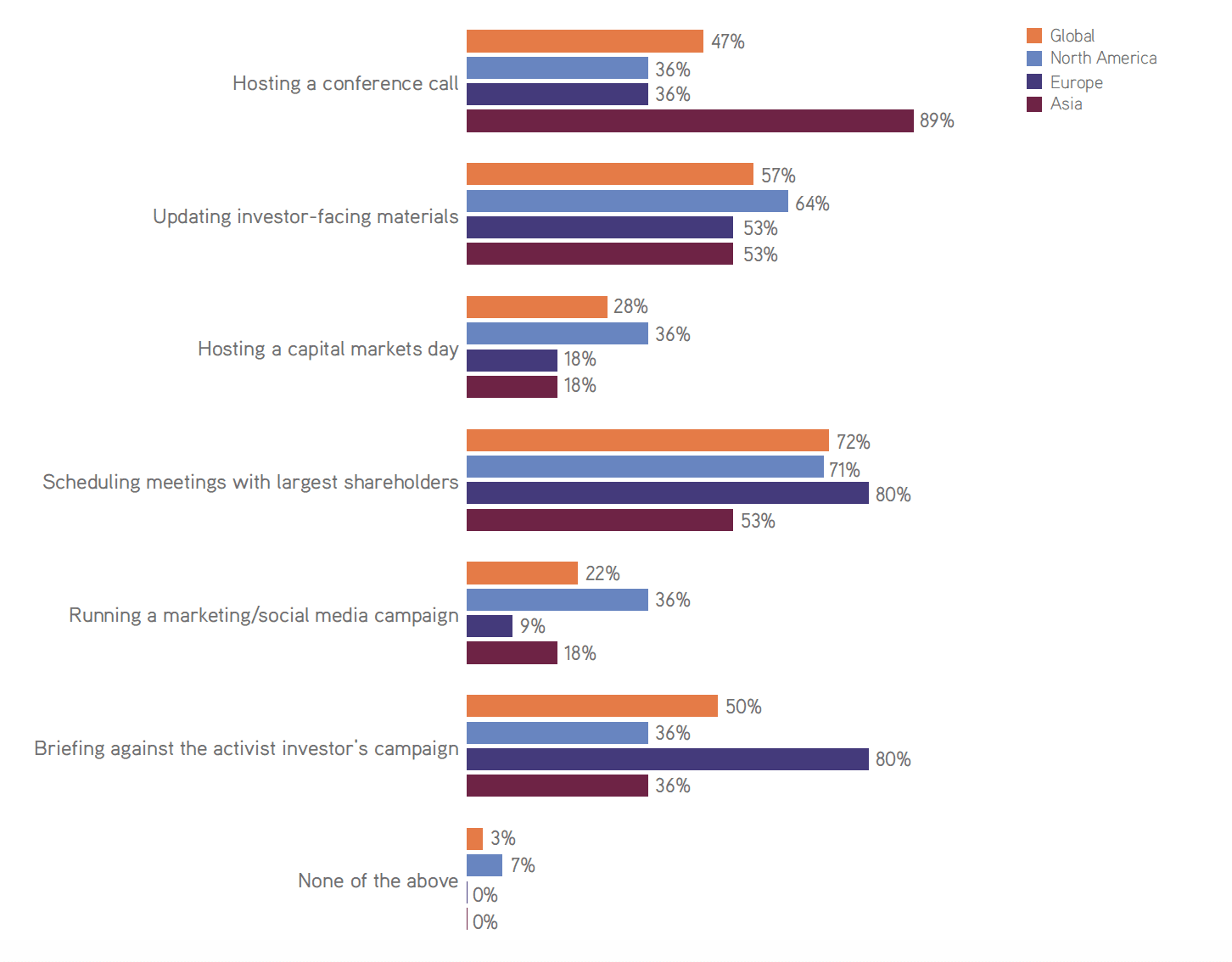

More than seven in 10 sell-side analysts expect companies to respond to an activist campaign by scheduling meetings with their major shareholders, while 57 percent expect them to update their investor-facing materials and half expect them to brief against the activist investor’s campaign.

Inaction is not an option according to most analysts, although having companies run a social media campaign or host a capital markets day are considered less relevant responses to an activist campaign against them.

There are notable regional differences in how analysts expect companies to respond to an activist campaign. Almost nine in 10 Asian analysts think it is important for companies to host a conference call in response, compared with 36 percent of North

American and European sell-siders. Eight in 10 European analysts think companies should respond by briefing against the activist investor, more than double the proportion of North American and Asian analysts who think the same. Asian analysts attach less importance than North American and European counterparts to scheduling a meeting with the company’s largest shareholders.

Sell side: How do you expect a company to respond when it is subject to a public shareholder activism campaign?